Can a Roofer Help With Insurance Claims

10min Read

10min Read

Posted 11.29.2025

Posted 11.29.2025

Can a Roofer Help with Insurance Claims?

Here’s a number that might make you spit out your coffee: 80% of homeowners who handle roof damage claims on their own end up with lower settlements than those who get professional help. That’s not a typo. If your roof just took a beating from one of Minnesota’s famous summer storms (or winter ice dams, or spring hail—take your pick), you’re probably wondering whether your insurance will actually cover the repairs. And more importantly, whether you’ll need a law degree to figure out the paperwork.

Good news: a roofer can absolutely help with your insurance claim. And honestly? It might be the smartest call you make during the whole process.

The Problem: Insurance Claims Are Designed to Be Confusing

Let’s be real—filing an insurance claim isn’t anyone’s idea of a good time. Between the adjuster visits, the documentation requirements, the industry jargon, and the back-and-forth phone calls, it’s easy to feel like you’re navigating a maze blindfolded. And that’s exactly when mistakes happen.

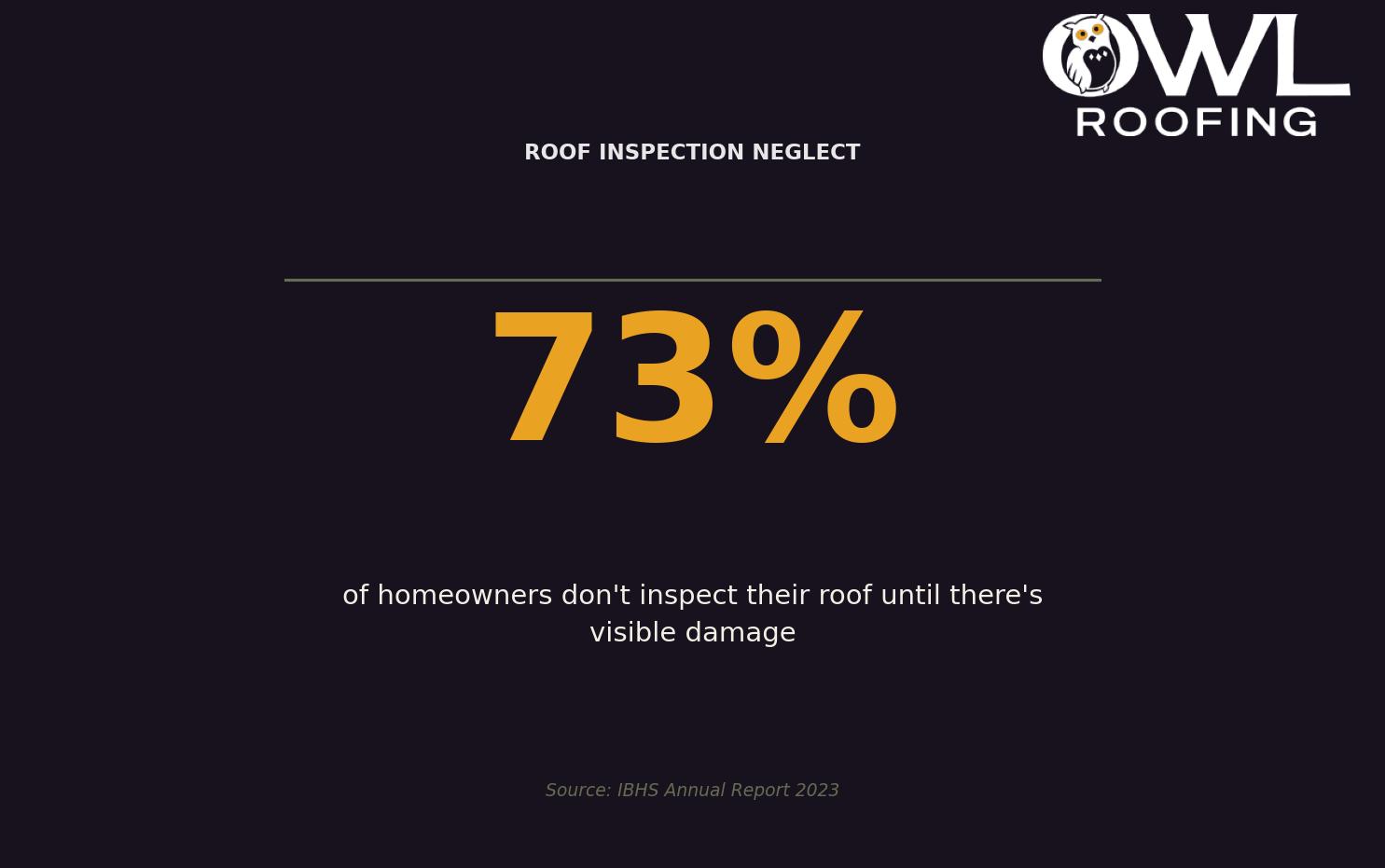

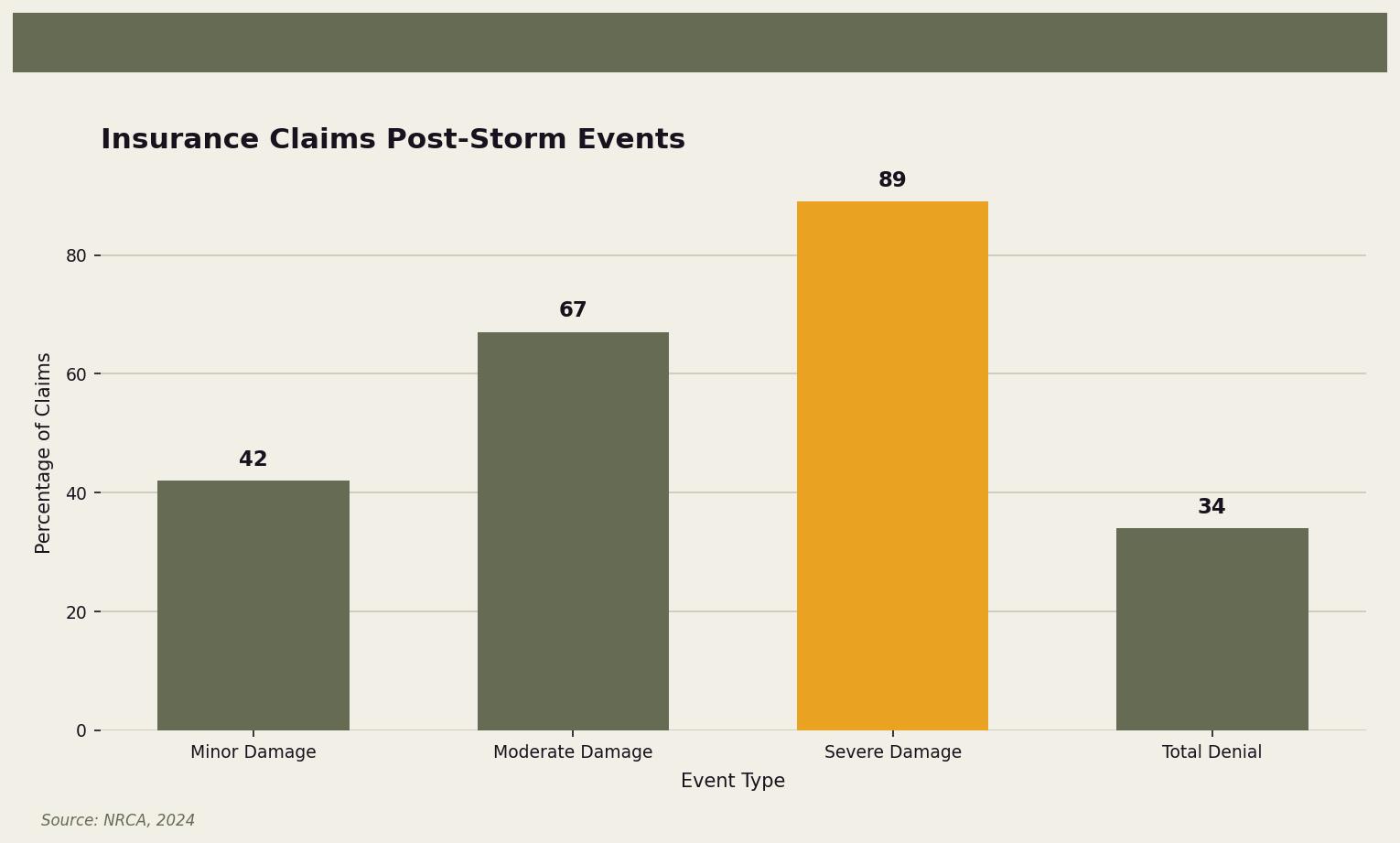

The National Roofing Contractors Association (NRCA) reports that 67% of homeowners face roofing issues after severe weather events. That’s two out of three homes in your neighborhood. Yet here’s the kicker from the Insurance Institute for Business & Home Safety (IBHS): 73% of homeowners don’t inspect their roofs until there’s visible damage inside their home—water stains on the ceiling, drips in the attic, that kind of thing.

By then, the damage has often spread far beyond what you can see. And if you don’t know what to look for, you won’t know what to claim. That’s money left on the table—your money.

The Consumer Federation of America has found that policyholders consistently receive lower settlements when they don’t utilize professional assistance. Translation: going it alone usually costs you.

The Promise: A Good Roofer Becomes Your Advocate

Here’s what a knowledgeable roofer actually does for your insurance claim: they become your translator, your documentarian, and your advocate all rolled into one.

They speak insurance. They know what adjusters look for. They understand which damage is claimable and how to present it in a way that gets approved rather than denied or underpaid. And they’ve seen enough storm damage to spot problems you’d never notice—the kind that cause major headaches two years down the road if they’re not addressed now.

This isn’t about gaming the system. It’s about making sure you get what you’re actually owed. You’ve been paying those premiums for years. When damage happens, you deserve a fair settlement.

How the Process Actually Works

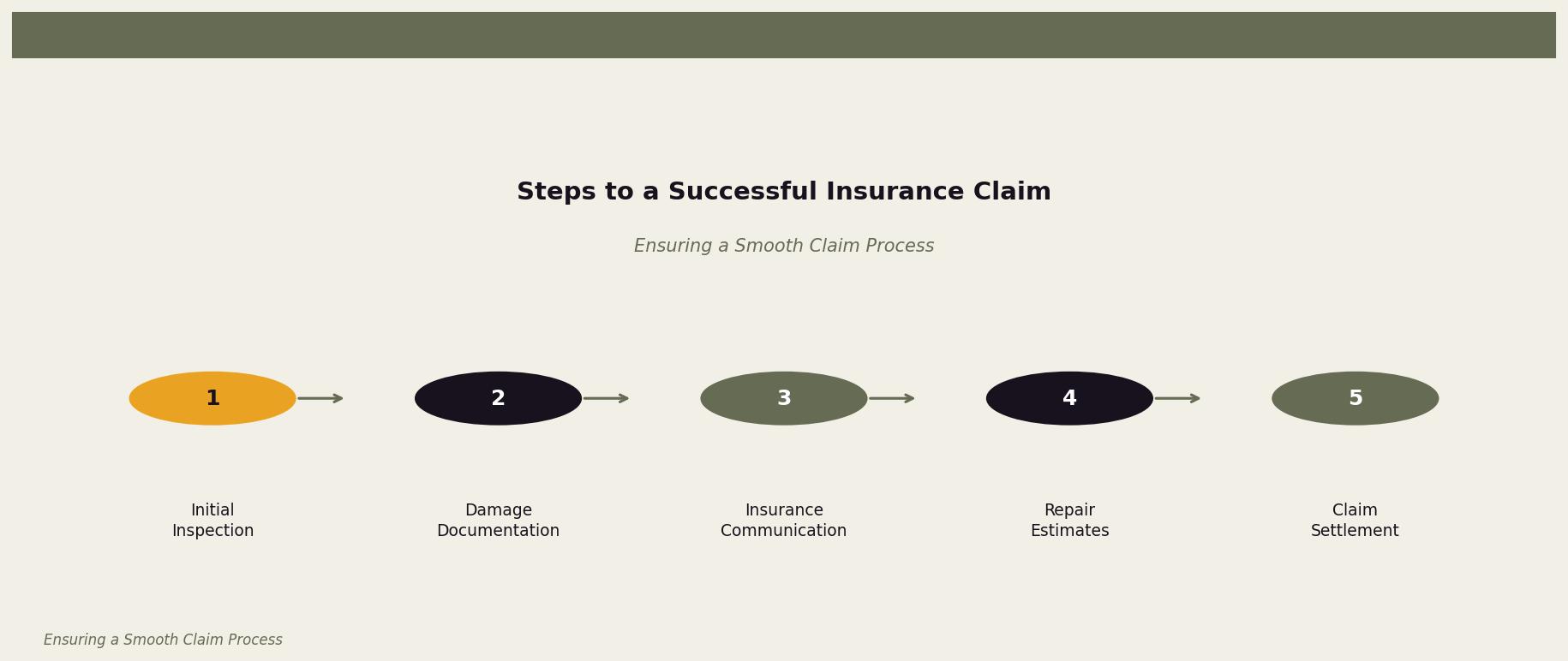

Step 1: The Inspection That Catches Everything

A skilled roofer starts with a thorough assessment—and we mean thorough. They’ll climb up there with a trained eye, checking for hail impacts, lifted shingles, cracked flashing, damaged vents, and all the subtle stuff that’s easy to miss from the ground.

They document everything with detailed photos and notes. This matters because insurance companies make decisions based on documentation. The more complete your evidence, the stronger your claim. Remember that IBHS stat—73% of homeowners wait until damage is visible inside. A proactive inspection catches problems early, before they become expensive emergencies.

Your roofer creates a comprehensive record: the type of damage, the extent, the affected areas, and what repairs are needed. This becomes the foundation of your entire claim.

Step 2: Translating “Roof Damage” into “Insurance Language”

Here’s where experience really pays off. Your roofer knows the terminology insurance companies expect. They know how to describe damage in terms adjusters understand and approve. They can prepare repair estimates that align with industry standards.

The NRCA emphasizes that clear communication between contractors and insurance companies significantly speeds up claim approvals. When everyone’s speaking the same language, there’s less back-and-forth, fewer delays, and fewer “we need more information” letters clogging up your mailbox.

Your roofer can also be present when the insurance adjuster visits. This is huge. They can point out damage the adjuster might miss, answer technical questions on the spot, and make sure nothing falls through the cracks.

Step 3: Negotiating When Needed

Sometimes insurance companies push back. They might dispute the extent of damage, question repair costs, or initially offer a settlement that doesn’t cover what’s actually needed. This is where having a roofer in your corner becomes invaluable.

They can provide supplemental documentation, explain why certain repairs are necessary, and advocate for a fair settlement based on their professional expertise. It’s not confrontational—it’s just making sure the numbers reflect reality.

DIY Claims vs. Professional Assistance: The Real Comparison

Going It Alone

Handling an insurance claim yourself might seem like the simpler route. Fewer people involved, right? But here’s what typically happens:

- You miss damage that isn’t obvious—cracked underlayment, compromised decking, damaged flashing around vents and chimneys

- Your documentation is incomplete, giving the insurance company reasons to reduce your settlement

- You don’t know what’s actually claimable versus what falls under “normal wear and tear”

- The back-and-forth drags on because you’re learning the process as you go

- You accept the first offer because you don’t know it’s negotiable

The result? Lower payouts, longer timelines, and repairs that might not fully address the problem.

Working with a Professional Roofer

The National Association of Realtors (NAR) reports that professionally assisted claims are settled more favorably 80% of the time compared to DIY attempts. That’s not a small edge—that’s a dramatic difference in outcomes.

With professional assistance, you get:

- Thorough documentation that leaves nothing out

- Expert opinions that carry weight with adjusters

- Someone who knows when a settlement offer is fair and when it’s not

- Faster resolution because the process runs smoother

- Peace of mind that your roof will actually be fixed right

Plus, you’re not spending your evenings trying to decode insurance policy language. That’s worth something.

Why This Matters Even More in Minnesota

Living in the Twin Cities means your roof deals with conditions most of the country never sees. We’re talking:

- Heavy snowfall that adds serious weight and moisture exposure

- Ice dams that form when heat escapes through your roof and melts snow that refreezes at the edges

- Freeze-thaw cycles that work their way into small cracks and make them big cracks

- Summer hail and wind that can shred shingles in minutes

- Temperature swings of 60+ degrees that stress roofing materials year after year

The Minnesota Department of Commerce processes hundreds of roofing claims annually, largely due to these conditions. And here’s the thing—damage from ice dams looks different than damage from hail, which looks different than damage from wind. A roofer who works in this climate year-round knows these patterns. They know what to look for after each type of weather event and how to document it in ways insurance companies recognize.

A roofer from Arizona wouldn’t know an ice dam if it fell on their head. Local experience matters.

Your Action Plan: What to Do After Storm Damage

If your roof just took a hit, here’s exactly what to do:

1. Document what you can safely see. Take photos from the ground of any obvious damage. Note the date and weather event. Don’t climb up there yourself—it’s not worth the risk.

2. Contact a reputable local roofer for a professional inspection. Look for someone with specific experience handling insurance claims, not just installing roofs. These are different skill sets.

3. File your claim promptly. Most policies have time limits for reporting damage. Don’t let paperwork anxiety cause you to miss deadlines.

4. Have your roofer present for the adjuster’s visit. This ensures all damage is identified and properly documented during the official inspection.

5. Review any settlement offer with your roofer before accepting. They can tell you whether it actually covers the necessary repairs.

6. Keep copies of everything. Every photo, every estimate, every email. If questions come up later, you’ll have answers.

The goal is simple: get your roof properly repaired without paying out of pocket for damage your insurance should cover. That requires being thorough from the start.

Ready to Get Your Claim Handled Right?

If you're dealing with roof damage in the Twin Cities, we'd love to help. At Owl Roofing, we've walked hundreds of homeowners through the insurance claim process—from that first inspection through final settlement. We know what Minnesota weather does to roofs because we live here too, right in Shoreview. We've seen hail damage and ice dam destruction and everything in between. We'll document everything, work directly with your insurance company, and make sure nothing gets missed. No pressure, no runaround—just honest help from neighbors who've done this many times before. Give us a call at 651-977-6027 or visit owlroofing.com/ to schedule an inspection. Protect Your Nest.

📍 Owl Roofing Serves the Entire Twin Cities Metro

Andover · Anoka · Apple Valley · Arden Hills · Big Lake · Blaine · Bloomington · Brooklyn Center · Brooklyn Park · Burnsville · Champlin · Chanhassen · Chaska · Columbia Heights · Coon Rapids · Cottage Grove · Crystal · deephaven · Delano · Eagan · East Bethel · Eden Prairie · Excelsior · Farmington · Forest Lake · Fridley · Golden Valley · Ham Lake · Hastings · Hopkins · Hugo · Inver Grove Heights · Lake Elmo · Lakeville · Lino Lakes · Mahtomedi · Maplewood · Mendota Heights · Minneapolis · Minnetrista · Mound · Mounds View · New Brighton · New Hope · North Oaks · North St. Paul · Oak Grove · Oakdale · Plymouth · Prior Lake · Ramsey · Richfield · Robbinsdale · Rosemount · Roseville · Saint Paul · Savage · Shakopee · Shoreview · South St. Paul · St. Louis Park · St. Michael · St. Paul · Stillwater · Vadnais Heights · Victoria · Waconia · wayzata · West St. Paul · White Bear Lake · woodbury

Licensed Minnesota roofing contractor · Free inspections · 10-year workmanship warranty · Get a free estimate →