Is a Roof Replacement Tax Deductible

9min Read

9min Read

Posted 11.14.2025

Posted 11.14.2025

Is a Roof Replacement Tax Deductible?

You just dropped $12,000 on a new roof. Now you’re staring at your tax return wondering: can I write any of this off? Here’s the honest answer most roofers won’t tell you—and the smarter money moves hiding in plain sight.

Every spring, Twin Cities homeowners shell out thousands to fix what winter destroyed. And every April, they Google the same question you’re asking right now. The rules are more nuanced than a simple yes or no, and knowing the difference could save you real money—either now or when you sell your house.

The Short Answer (And Why It’s Not That Simple)

Let’s cut to it: a standard roof replacement is not tax deductible for most homeowners. The IRS classifies it as a “capital improvement,” not a repair. That distinction matters.

A repair fixes something broken—patching a leak, replacing a few shingles after a storm. The IRS lets you deduct repairs on rental properties, but for your primary residence? Not so much.

An improvement adds value or extends your home’s life. A full roof replacement falls into this bucket. You can’t deduct it from this year’s income taxes like you would mortgage interest or property taxes.

But here’s where it gets interesting—and where most articles stop too soon.

The Hidden Tax Benefit Most Homeowners Miss

Your new roof isn’t a write-off, but it’s not worthless on your taxes either. It increases your home’s “adjusted cost basis.” That’s accountant-speak for: it reduces how much profit the IRS thinks you made when you eventually sell.

Here’s how it works:

Say you bought your home for $300,000. Over the years, you put $40,000 into improvements—new roof, updated kitchen, finished basement. Your adjusted basis is now $340,000. When you sell for $450,000, your taxable gain is $110,000 instead of $150,000.

With capital gains rates ranging from 0% to 20% depending on your income, that $40,000 in improvements could save you $8,000 or more in taxes. Not pocket change.

The catch? You need documentation. Every receipt. Every contract. Every invoice. Keep them somewhere you’ll actually find them in 10 years. Your future self will thank you.

The Energy Efficiency Loophole That Actually Works

Now here’s where it gets good for Twin Cities homeowners planning ahead.

The federal government really wants you to make your home more energy efficient. So much so that they’ll give you actual tax credits—dollar-for-dollar reductions in what you owe—for certain roofing materials.

This isn’t a deduction (which just reduces your taxable income). A credit directly cuts your tax bill. A $500 credit means $500 less you pay to the IRS. Period.

What Qualifies for the Energy Efficient Home Improvement Credit

Under current IRS guidelines, you can claim credits for roofing products that meet ENERGY STAR requirements. We’re talking about:

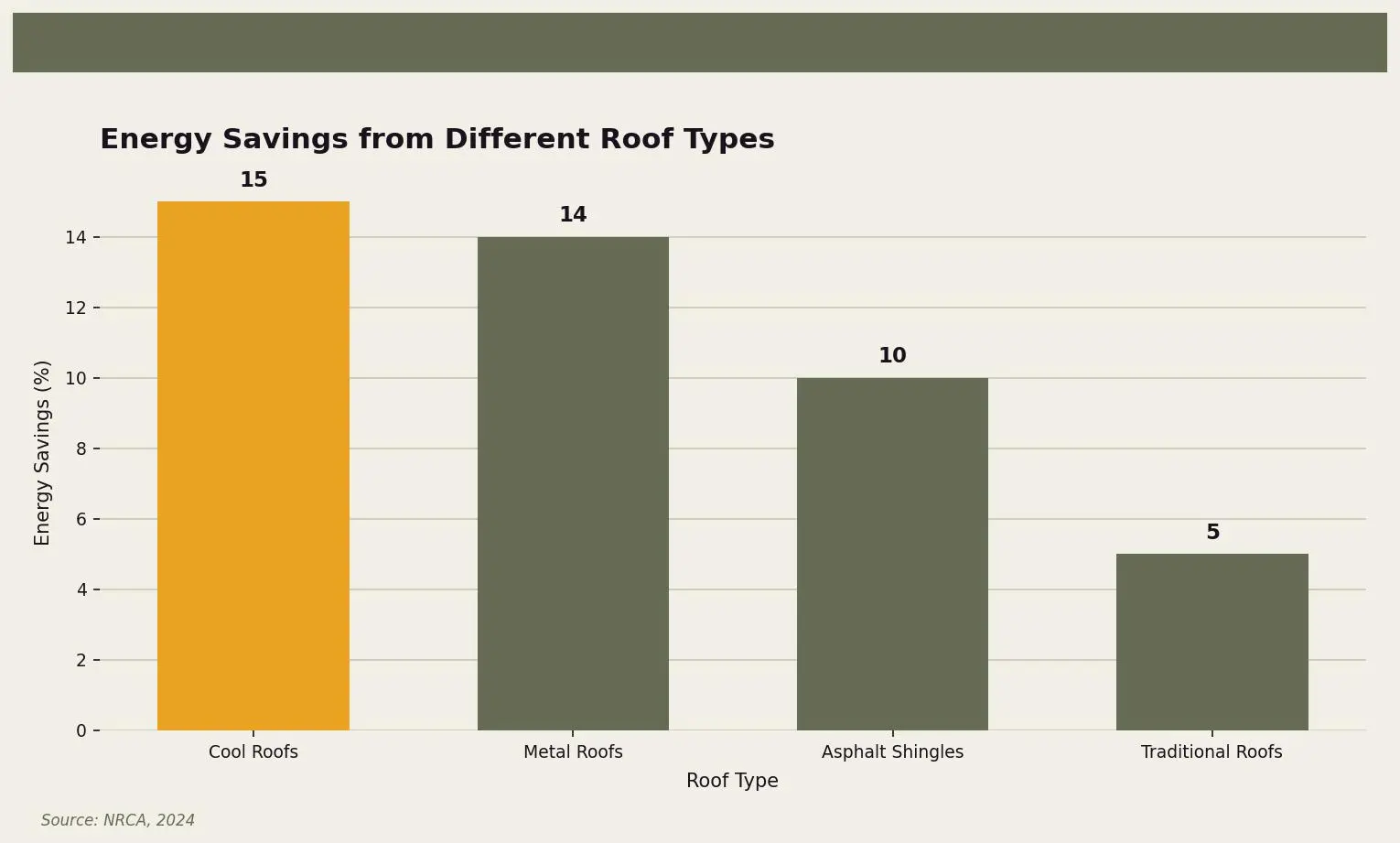

- Metal roofs with pigmented coatings: These reflect solar heat and can last 50+ years according to NRCA data. They’re especially smart for south-facing roofs that bake in summer.

- Asphalt shingles with cooling granules: Not all shingles qualify—only those meeting specific reflectivity standards. Ask your contractor for ENERGY STAR certified options.

- Cool roofs: Designed to reflect more sunlight and absorb less heat. The Insurance Institute for Business & Home Safety (IBHS) reports these can cut cooling costs by up to 15%.

The credit typically covers 30% of material costs (not installation), up to annual and lifetime limits. For 2024, you’re looking at up to $1,200 for roofing materials specifically. Check IRS Form 5695 for current limits—these change periodically.

Why This Matters More in Minnesota

You might think “cool roofs” are a sunbelt thing. Why would a Shoreview homeowner care about reflecting solar heat when we’re scraping ice off our cars six months a year?

Two reasons:

First, our summers are getting hotter. Those July weeks when your AC runs nonstop? An energy-efficient roof keeps your attic cooler, so your whole house stays more comfortable. NRCA data shows energy-efficient roofs can save homeowners up to 15% on annual heating and cooling costs combined.

Second, many of these materials also perform better in our brutal freeze-thaw cycles. Metal roofs shed snow and ice. Quality asphalt shingles with modern technology resist cracking when temperatures swing 60 degrees in a week (because Minnesota).

The Minnesota Department of Commerce has found that homes with energy-efficient features sell 3% faster than comparable homes without them. In a competitive market, that edge matters.

Special Cases: When Your Roof IS Deductible

There are a few situations where the rules change:

If You Have a Home Office

Use part of your home exclusively and regularly for business? You might deduct a percentage of roof costs proportional to your office space. If your home office is 10% of your home’s square footage, you could potentially deduct 10% of that roof replacement.

Fair warning: home office deductions are audit magnets. Make sure you legitimately qualify and document everything. Talk to a tax professional before claiming this.

If You Rent Out Part of Your Home

Got a duplex? Rent out your basement apartment? The roof costs associated with the rental portion may be deductible or depreciable. Again, this gets complicated fast—consult a CPA who knows rental property rules.

If You’re a Landlord

For investment properties, roof replacement is typically depreciated over 27.5 years (residential) or 39 years (commercial). You can’t deduct the whole cost in year one, but you get to chip away at it annually. Some situations may qualify for bonus depreciation or Section 179 treatment—your accountant will know.

Storm Damage: A Different Ballgame

Did a hailstorm or fallen tree take out your roof? The tax situation differs here too.

If insurance covers the damage, you generally can’t deduct anything—you’ve been made whole. But if your out-of-pocket costs exceed insurance payouts, you might have a casualty loss deduction available.

The rules tightened considerably after 2017’s tax reform. Now, casualty losses on personal residences are only deductible if they’re in a federally declared disaster area. Minnesota sees these declarations periodically after major storms, so it’s worth checking if your timing aligns.

The Real Cost of Waiting: A Quick Reality Check

Here’s something the tax code won’t tell you: delaying a needed roof replacement to “save money” often backfires spectacularly.

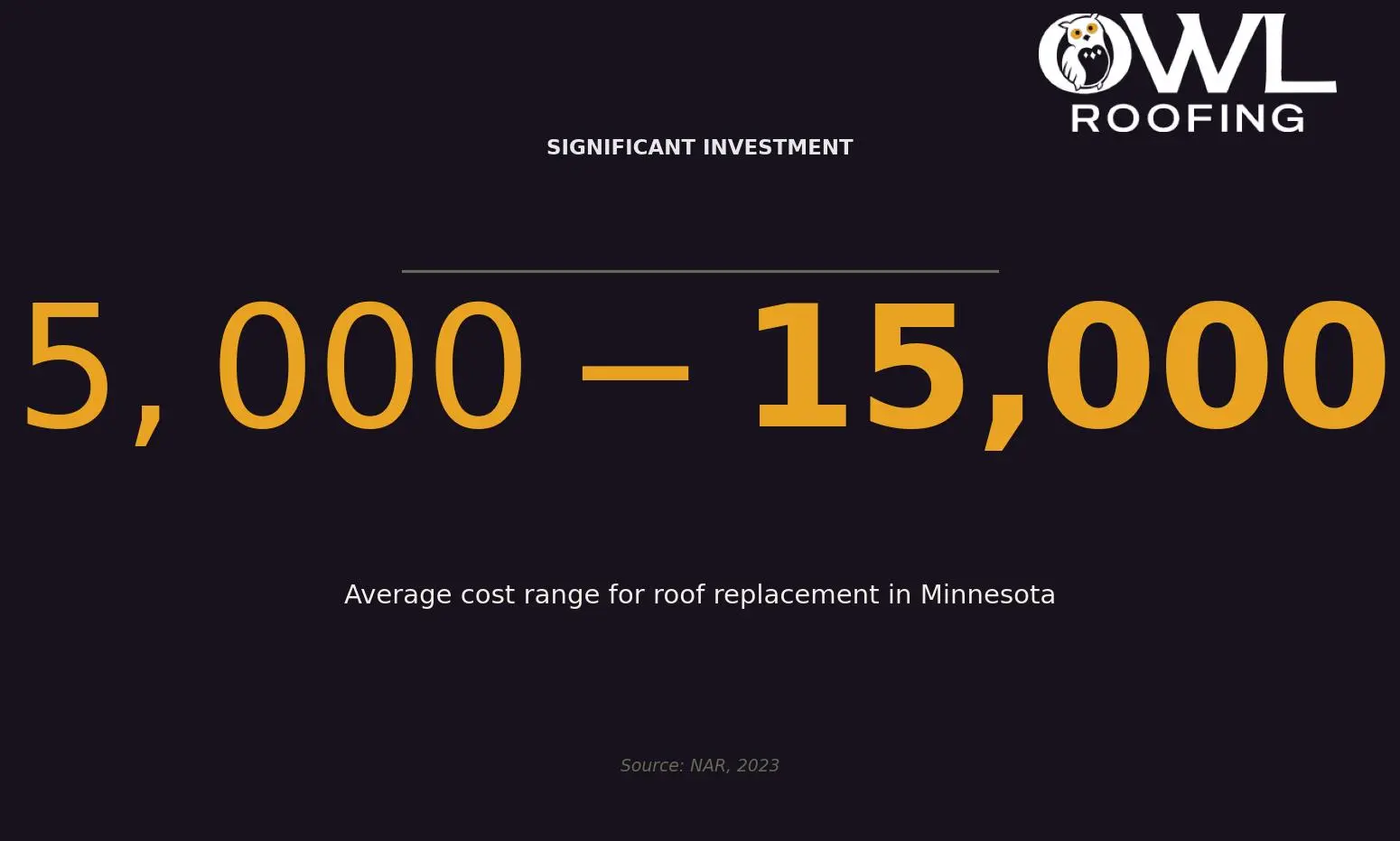

The National Association of Realtors puts the average Minnesota roof replacement between $5,000 and $15,000. That’s a big range, and where you land depends largely on material choices and roof complexity.

But waiting until your roof fails? Now you’re paying for:

- Emergency service premiums (contractors charge more when you need them yesterday)

- Interior damage repairs (water doesn’t stop at the attic)

- Mold remediation (Minnesota humidity plus water intrusion equals expensive problems)

- Temporary housing if damage is severe

A planned replacement with time to compare quotes, select energy-efficient materials that qualify for credits, and schedule installation during a slower season? That’s how you actually save money—tax benefits or not.

Your Action Plan: Making This Work for You

Ready to turn this information into actual savings? Here’s your checklist:

Before you replace your roof:

- Get multiple quotes and ask specifically about ENERGY STAR certified materials

- Request itemized estimates separating materials from labor (credits apply to materials only)

- Ask contractors which products qualify for federal tax credits

- Check Minnesota’s current energy efficiency incentives—these change and sometimes stack with federal credits

During installation:

- Keep every receipt, contract, and manufacturer certification

- Take dated photos of the work

- Get written confirmation that materials meet ENERGY STAR requirements

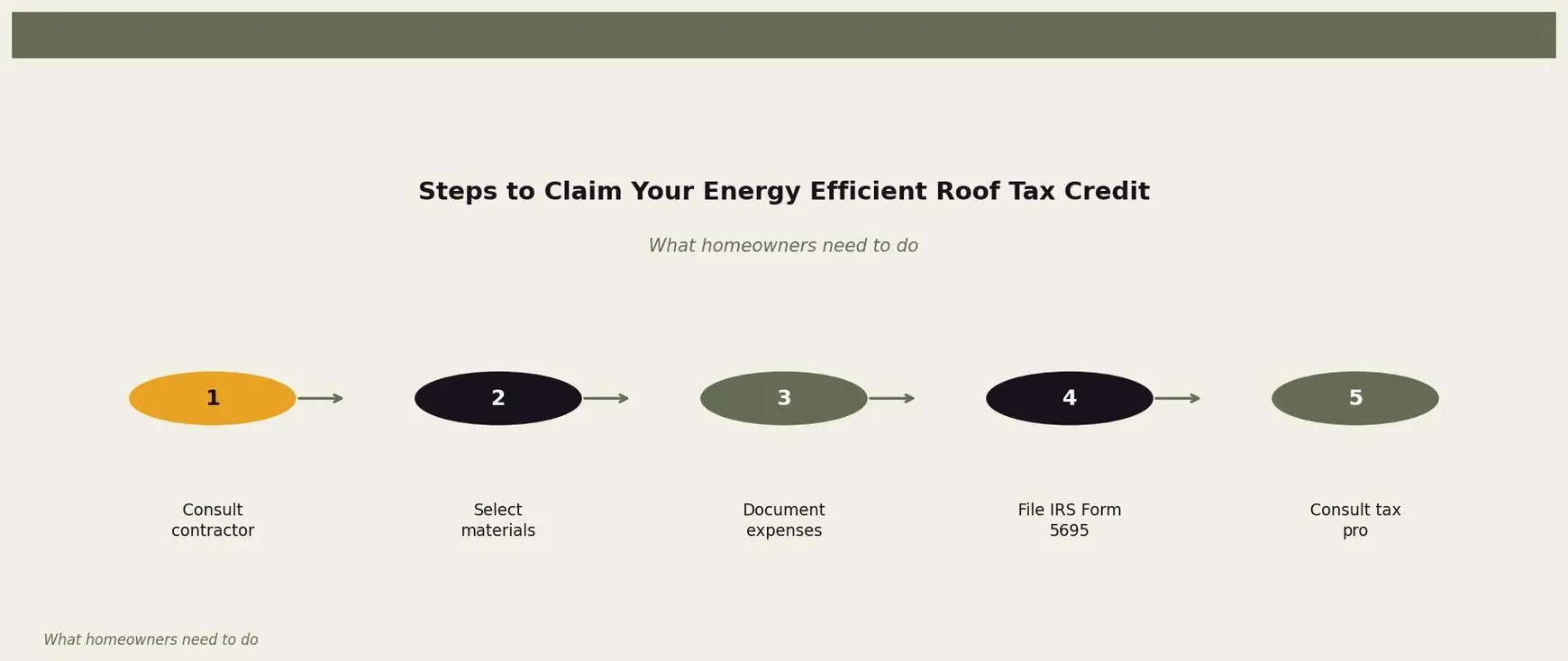

At tax time:

- Use IRS Form 5695 to claim the Residential Clean Energy Credit or Energy Efficient Home Improvement Credit

- Add the full improvement cost to your home’s basis documentation

- Consult a tax professional if you have rental property, home office, or storm damage complications

Ready to Talk About Your Roof?

Taxes are complicated. Roofs don’t have to be.

At Owl Roofing, we’ve helped hundreds of Twin Cities homeowners navigate exactly these decisions. We’re based right here in Shoreview—not a franchise, not storm chasers, just neighbors who know Minnesota roofs inside and out. We’ll walk you through which materials make sense for your home and budget, including options that qualify for energy efficiency credits. No pressure, no confusing estimates, just straight answers from people who’ll still be here when you need us.

Give us a call at 651-977-6027 or visit owlroofing.com/ to schedule a free inspection. We’ll tell you exactly what your roof needs—and what it doesn’t.

Protect Your Nest.

📍 Owl Roofing Serves the Entire Twin Cities Metro

Andover · Anoka · Apple Valley · Arden Hills · Big Lake · Blaine · Bloomington · Brooklyn Center · Brooklyn Park · Burnsville · Champlin · Chanhassen · Chaska · Columbia Heights · Coon Rapids · Cottage Grove · Crystal · deephaven · Delano · Eagan · East Bethel · Eden Prairie · Excelsior · Farmington · Forest Lake · Fridley · Golden Valley · Ham Lake · Hastings · Hopkins · Hugo · Inver Grove Heights · Lake Elmo · Lakeville · Lino Lakes · Mahtomedi · Maplewood · Mendota Heights · Minneapolis · Minnetrista · Mound · Mounds View · New Brighton · New Hope · North Oaks · North St. Paul · Oak Grove · Oakdale · Plymouth · Prior Lake · Ramsey · Richfield · Robbinsdale · Rosemount · Roseville · Saint Paul · Savage · Shakopee · Shoreview · South St. Paul · St. Louis Park · St. Michael · St. Paul · Stillwater · Vadnais Heights · Victoria · Waconia · wayzata · West St. Paul · White Bear Lake · woodbury

Licensed Minnesota roofing contractor · Free inspections · 10-year workmanship warranty · Get a free estimate →