What Roof Damage Is Covered by Insurance

13min Read

13min Read

Posted 11.27.2025

Posted 11.27.2025

What Roof Damage is Covered by Insurance?

Last summer, a nasty hailstorm tore through Shoreview in about twelve minutes flat. The next morning, half the neighborhood was standing in their driveways, coffee in hand, staring at shingles in the bushes. The question on everyone’s mind? “Is this going to cost me five grand, or is insurance picking up the tab?”

Here’s the thing: most Twin Cities homeowners have no idea what their insurance actually covers until they need it. And by then, you’re stressed, possibly dealing with a leak, and definitely not in the mood to decode policy jargon. So let’s break this down before the next storm rolls through — because in Minnesota, there’s always a next storm.

Why Understanding Your Coverage Actually Matters

Your roof isn’t just shingles and nails. It’s the barrier between your family and everything Minnesota throws at you — blizzards, hail, wind, that random ice storm in April when you thought spring had finally arrived. When your roof takes a hit, the damage doesn’t stay on the surface. Water finds its way in. Then comes the mold, the ruined insulation, the ceiling stains, and eventually, structural problems that make a roof replacement look cheap by comparison.

The National Roofing Contractors Association (NRCA) puts it simply: understanding your insurance policy and staying on top of maintenance can save you from surprise five-figure expenses. That’s not scare tactics — that’s just math. A typical roof replacement in the Twin Cities runs anywhere from $8,000 to $25,000 depending on size and materials. Knowing what your insurance will and won’t cover before disaster strikes? That’s the difference between a stressful week and a financial crisis.

According to the Insurance Information Institute, homeowners insurance policies typically cover roof damage caused by unpreventable incidents like storms or fires. But “typically” is doing a lot of heavy lifting in that sentence. The details matter, and they vary from policy to policy. Let’s get specific.

Types of Roof Damage Your Insurance Will Likely Cover

Storm Damage: The Big One for Minnesota

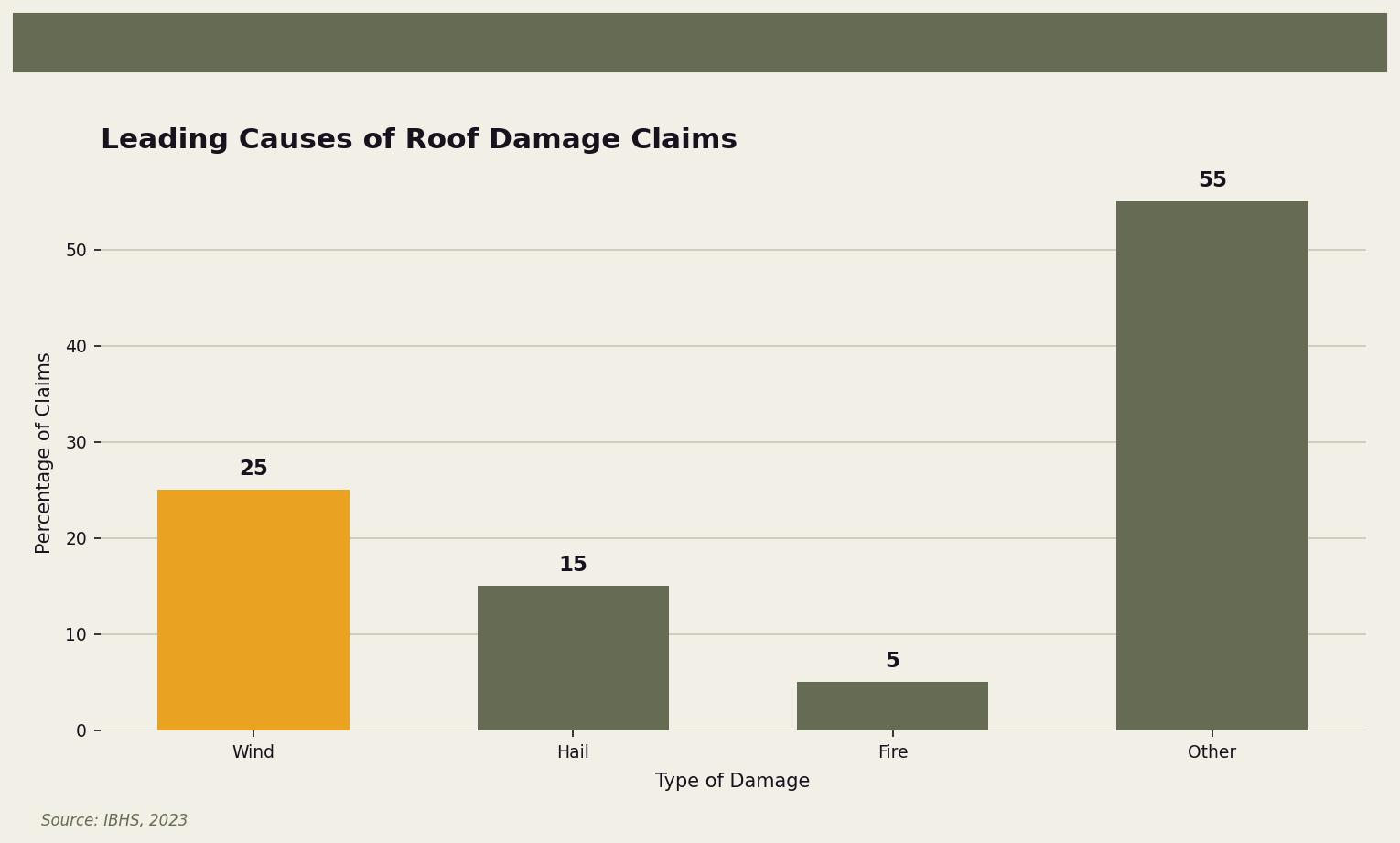

If you’ve lived in the Twin Cities for more than a year, you’ve probably experienced at least one storm that made you wonder if your roof was still attached. Good news: storm damage is almost always covered by standard homeowners insurance policies. We’re talking wind, hail, lightning, falling trees — the dramatic stuff.

The Insurance Institute for Business & Home Safety (IBHS) reports that wind and hail damage account for nearly 40% of all homeowners insurance claims filed annually. That’s not surprising when you consider that Minnesota averages about 30 hail days per year, with some of those storms dropping golf-ball-sized ice on your shingles.

Here’s what typically qualifies for coverage:

- Wind damage: Missing shingles, lifted edges, exposed underlayment, or debris punctures

- Hail damage: Dents, cracks, granule loss, or bruised shingles (even if you can’t see it from the ground)

- Lightning strikes: Direct hits that damage roofing materials or cause fires

- Fallen trees or branches: As long as the tree was healthy and the fall was caused by a storm

One important catch: your roof needs to have been in reasonable condition before the storm hit. If your 25-year-old shingles were already curling and cracked, your insurer might argue the storm just finished what neglect started. We’ll get to that.

Fire Damage: Covered, No Questions Asked

Fire is one of the “named perils” that virtually every homeowners policy covers without much debate. Whether it’s a wildfire (increasingly relevant even here in Minnesota), a lightning strike, a chimney fire, or an electrical issue that spreads to your roof, your insurance should cover repair or replacement costs.

The National Association of Realtors (NAR) confirms that most standard policies cover fire damage because it’s sudden and accidental — two words insurance companies love. Unlike gradual damage that develops over time, a fire is an event with a clear before and after. That makes the claim process more straightforward.

Weight of Ice, Snow, or Sleet

This one’s particularly relevant for Minnesota homeowners. If a heavy snow load causes your roof to sag, crack, or collapse, that’s typically covered. Same goes for ice damage — though ice dams themselves get complicated (more on that in a minute). The key is that the damage has to be from the weight or impact of winter weather, not from water that gradually seeped in because your attic wasn’t ventilated properly.

Vandalism and Falling Objects

Less common, but worth knowing: if someone damages your roof intentionally, or if something unexpected falls on it (a satellite dish from a neighbor’s house, debris from a construction site, even a small aircraft), your insurance generally covers the repairs. These fall under “sudden and accidental” damage, which is the magic phrase in insurance land.

Types of Roof Damage Your Insurance Won’t Cover

Wear and Tear: The Slow Decline

Here’s where a lot of homeowners get tripped up. Insurance is designed to protect you from unexpected events — not from the predictable reality that roofs age and eventually need replacement. A 20-year-old roof with curling shingles, granule loss, and general weathering? That’s not storm damage. That’s just… time.

The NRCA emphasizes regular maintenance to prolong your roof’s life and catch problems before they become emergencies. Your insurer expects you to do the same. If an adjuster shows up after a storm and sees years of accumulated neglect, they’re going to attribute the damage to wear and tear — and deny your claim.

Poor Maintenance: The Claim Killer

This is related to wear and tear but deserves its own callout because it’s so common. The IBHS reports that 73% of homeowners don’t inspect their roofs until there’s visible damage. That’s a problem, because “visible damage” often means the problem started months or years ago.

Examples of maintenance issues that can get your claim denied:

- Clogged gutters that caused water backup and rotted fascia

- Missing or damaged flashing around chimneys and vents that was never repaired

- Moss or algae growth that was left to spread and deteriorate shingles

- Small leaks that were ignored until they became big leaks

The rule of thumb: if a reasonable homeowner would have noticed and fixed the problem before it got bad, your insurer will expect you to have done the same.

Cosmetic Damage: It Looks Bad, But…

Some policies exclude “cosmetic damage” — meaning damage that affects appearance but not function. Hail dents on metal roofing, for example, might not be covered if the roof still keeps water out. This is policy-specific, so read your coverage carefully or ask your agent directly.

Flood Damage: The Big Exclusion

Standard homeowners insurance does not cover flood damage. Period. If rising water damages your roof from below (unlikely) or if flood-related debris damages your roof (more plausible), you’d need separate flood insurance. This matters less for roof-specific claims, but it’s worth knowing as part of your overall coverage picture.

The Minnesota Angle: Ice Dams and Freeze-Thaw Cycles

Let’s talk about the unique joy of Minnesota homeownership: ice dams. If you’ve never experienced one, here’s the short version. Heat escapes from your attic, melts snow on your roof, and that water runs down to the colder edges where it refreezes. Over time, you get a ridge of ice at your roofline that traps water behind it. That trapped water backs up under your shingles and into your home.

Insurance coverage for ice dam damage is… complicated. Many policies cover the resulting water damage (ruined ceilings, wet insulation, mold remediation) but not the cost of removing the ice dam itself or fixing the underlying ventilation issues that caused it. The Minnesota Department of Commerce advises homeowners to keep gutters clean and ensure proper attic insulation to minimize ice dam formation in the first place.

The freeze-thaw cycle also takes a toll on roofing materials over time. Water gets into small cracks, freezes, expands, and makes those cracks bigger. Repeat this a hundred times over a Minnesota winter, and you’ve got deterioration that insurance won’t cover because it happened gradually.

Prevention is your best friend here. Proper attic ventilation, adequate insulation, and regular inspections after winter can catch problems before they become claim-worthy emergencies that your insurer might not cover anyway.

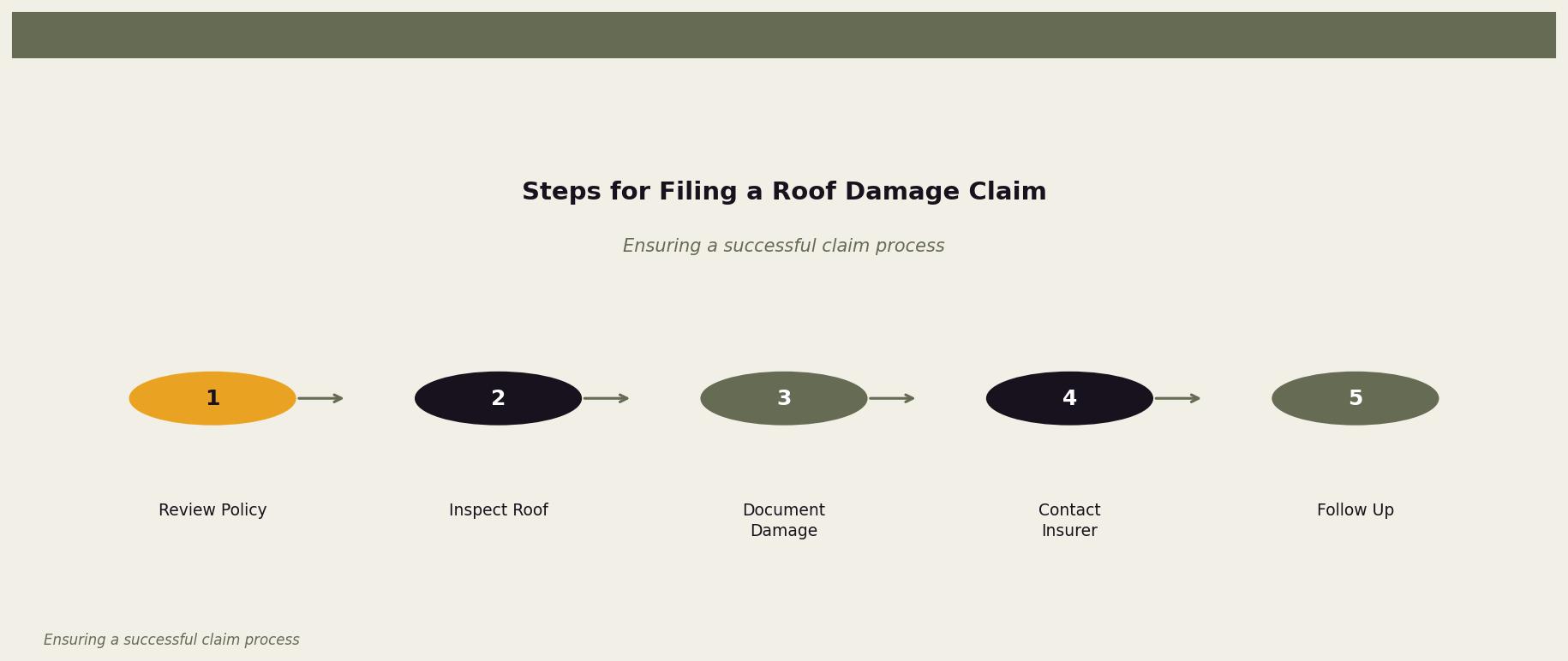

How to File a Roof Damage Claim (And Actually Get Paid)

Okay, so a storm hit, your roof took damage, and you’re pretty sure it’s covered. Here’s how to handle the claim process without losing your mind:

Step 1: Review Your Policy First

Step 2: Document Everything

Take photos. Lots of photos. From the ground, from a ladder if you can do it safely, and from any interior spaces where damage is visible. Date-stamp everything. If you have photos of your roof before the damage (from a previous inspection or real estate listing), even better. The more evidence you have, the smoother your claim will go.

Step 3: Get a Professional Inspection

A reputable roofing contractor can assess the damage and provide a detailed report that supports your claim. They’ll catch damage you might miss — like hail bruises that aren’t visible from ground level but will cause leaks within a year or two. This inspection is also your chance to get an estimate you can compare to whatever your insurance adjuster comes up with.

Step 4: Contact Your Insurance Company Promptly

Most policies require you to report damage within a reasonable timeframe. Don’t wait weeks to call. File your claim, get a claim number, and ask about their process and timeline. Some insurers send their own adjusters; others accept contractor estimates. Know what to expect.

Step 5: Be Present for the Adjuster’s Visit

When the insurance adjuster comes out, be there. Walk them through the damage. Share your documentation. If your contractor can be there too, even better — they can point out damage the adjuster might miss and advocate for a fair assessment.

Step 6: Don’t Accept the First Offer If It’s Wrong

Insurance adjusters aren’t trying to cheat you, but they’re also not incentivized to maximize your payout. If their estimate seems low compared to what reputable contractors are quoting, push back. Request a re-inspection. Provide additional documentation. You have the right to dispute a low settlement.

Protect Your Coverage Before You Need It

The best time to deal with insurance questions is before you have a claim. Here are a few things you can do right now to make sure you’re covered when it counts:

- Schedule annual roof inspections. A professional can catch small problems before they become big ones — and give you documentation of your roof’s condition.

- Keep maintenance records. If you’ve replaced flashing, cleaned gutters, or repaired small issues, save the receipts and photos. This proves you’ve been a responsible homeowner.

- Photograph your roof after it’s installed or repaired. These “before” photos can be crucial if you ever need to prove damage happened suddenly.

- Review your policy annually. Coverage changes. Your roof ages. Make sure your policy still makes sense for your situation.

- Consider your deductible. A higher deductible means lower premiums, but it also means more out-of-pocket costs when you file a claim. Find the balance that works for your budget.

Let’s Talk About Your Roof

If you’re reading this after a storm — or just because you realized you haven’t thought about your roof in a while — we’d be happy to help. At Owl Roofing, we’re based right here in Shoreview and serve homeowners across the Twin Cities. We’ve seen every type of roof damage Minnesota weather can dish out, and we’ve helped plenty of our neighbors navigate the insurance process.

We’ll give you an honest assessment of what’s going on up there. If it’s something insurance should cover, we’ll document it properly and work with your adjuster. If it’s maintenance you’ve been putting off, we’ll tell you that too — no pressure, no upselling. Just straight answers from people who live in the same community and deal with the same weather you do.

Give us a call at 651-977-6027 or visit owlroofing.com/ to schedule an inspection. We’re Tim, Bea, Noah, and Anya — and we’re here when you need us.

Protect Your Nest.

📍 Owl Roofing Serves the Entire Twin Cities Metro

Andover · Anoka · Apple Valley · Arden Hills · Big Lake · Blaine · Bloomington · Brooklyn Center · Brooklyn Park · Burnsville · Champlin · Chanhassen · Chaska · Columbia Heights · Coon Rapids · Cottage Grove · Crystal · deephaven · Delano · Eagan · East Bethel · Eden Prairie · Excelsior · Farmington · Forest Lake · Fridley · Golden Valley · Ham Lake · Hastings · Hopkins · Hugo · Inver Grove Heights · Lake Elmo · Lakeville · Lino Lakes · Mahtomedi · Maplewood · Mendota Heights · Minneapolis · Minnetrista · Mound · Mounds View · New Brighton · New Hope · North Oaks · North St. Paul · Oak Grove · Oakdale · Plymouth · Prior Lake · Ramsey · Richfield · Robbinsdale · Rosemount · Roseville · Saint Paul · Savage · Shakopee · Shoreview · South St. Paul · St. Louis Park · St. Michael · St. Paul · Stillwater · Vadnais Heights · Victoria · Waconia · wayzata · West St. Paul · White Bear Lake · woodbury

Licensed Minnesota roofing contractor · Free inspections · 10-year workmanship warranty · Get a free estimate →