How Long Do You Have to File a Roof Claim

12min Read

12min Read

Posted 11.28.2025

Posted 11.28.2025

How Long Do You Have to File a Roof Claim?

That hailstorm last June? The one that woke up half of Shoreview at 2 AM? Your neighbor already got their roof replaced. But you’ve been busy. Life happened. And now you’re staring at your ceiling in March, noticing a water stain that definitely wasn’t there before, wondering: did I miss my chance to file a claim?

Here’s the uncomfortable truth — you might have. And that roof claim deadline isn’t something your insurance company is going to remind you about.

Every year, Twin Cities homeowners lose thousands of dollars because they didn’t know the clock was ticking. They assumed they had plenty of time. They figured they’d “deal with it later.” And then later became too late.

But it doesn’t have to be that way. Once you understand exactly how these deadlines work — and what steps to take right now — you can stop worrying and start protecting your home (and your wallet). Let’s break it down.

Why the Roof Claim Deadline Actually Matters

We get it. Filing insurance claims isn’t exactly anyone’s idea of a good time. There’s paperwork, phone calls, adjusters poking around your property. Easy to put off until “next weekend.”

But here’s what’s at stake: the Insurance Information Institute reports that weather-related claims make up about half of all homeowner insurance claims, with roof damage leading the pack. And in Minnesota? Our roofs take an absolute beating.

We’re talking ice dams in January, hail in June, wind damage year-round, and the constant freeze-thaw cycles that slowly destroy shingles from the inside out. Your roof isn’t just sitting up there — it’s fighting a war every single season.

Miss your filing window, and you’re looking at paying for that battle damage yourself. No partial coverage. No negotiation. Just a denial letter and a repair bill that could easily hit five figures.

That’s why understanding your roof claim deadline isn’t just administrative busywork — it’s the difference between a covered repair and a financial headache you didn’t see coming.

Understanding Your Roof Claim Deadline

So… How Long Do You Actually Have?

Here’s where it gets tricky: there’s no single answer. Your roof insurance claim time limit depends entirely on your specific policy and insurance provider.

The general range? Most insurers require claims to be filed within one year from the date of damage. But — and this is a big but — some policies slash that window down to just 60 days. Two months. That summer hailstorm could already be outside your filing window by the time the leaves change color.

The National Roofing Contractors Association (NRCA) recommends reviewing your policy annually, specifically looking for these deadline clauses. They’re often buried in the fine print, sandwiched between sections about liability limits and deductible structures. Not exactly beach reading, but absolutely worth knowing.

Here’s a quick breakdown of what we typically see in the Twin Cities:

- Standard policies: 12-month filing window from date of damage

- Stricter policies: 6-month window (increasingly common after major storm seasons)

- Most restrictive policies: 60-90 day windows (usually with budget carriers)

Don’t assume you know your deadline. Pull out your policy documents tonight and find that number. Or call your agent tomorrow and ask directly. This is one of those things where guessing can cost you thousands.

What Happens If You Miss the Deadline?

Nothing good.

A missed filing deadline typically results in a flat-out denied claim. No appeals process. No exceptions because you were “really busy” or “didn’t notice the damage right away.” Insurance companies are remarkably unsympathetic about this stuff — and legally, they don’t have to be.

The financial hit? According to the Insurance Institute for Business & Home Safety (IBHS), moderate roof repairs average between $5,000 and $10,000. Full replacements in the Twin Cities often run $15,000 to $30,000 depending on your roof size and materials. That’s a lot of money to leave on the table because of a missed deadline.

But wait — it gets worse. A denied claim due to a missed deadline can also:

- Affect your future insurance premiums

- Impact your coverage eligibility when you try to renew or switch carriers

- Create complications if you try to sell your home (buyers and their inspectors ask questions)

The ripple effects extend way beyond that initial repair bill. This is why acting quickly isn’t just smart — it’s essential.

The Details: Deadlines, Regulations, and Processing Times

Minnesota’s Rules (Or Lack Thereof)

Here’s something that surprises a lot of homeowners: Minnesota doesn’t impose a state-mandated deadline for filing roof claims. The state leaves it entirely up to individual insurance companies to set their own policies.

This means your neighbor with State Farm might have a completely different deadline than you have with Travelers. A comparative analysis by the National Association of Realtors (NAR) shows significant variation between carriers — some offer that generous one-year window, while others enforce much stricter timelines, especially in the aftermath of major weather events like the hailstorms that regularly pummel the metro area.

After a big storm, some insurers even temporarily tighten their filing requirements. They know claims are coming, and they’re looking for any legitimate reason to reduce their payouts. Don’t give them one.

How Long Does the Claims Process Actually Take?

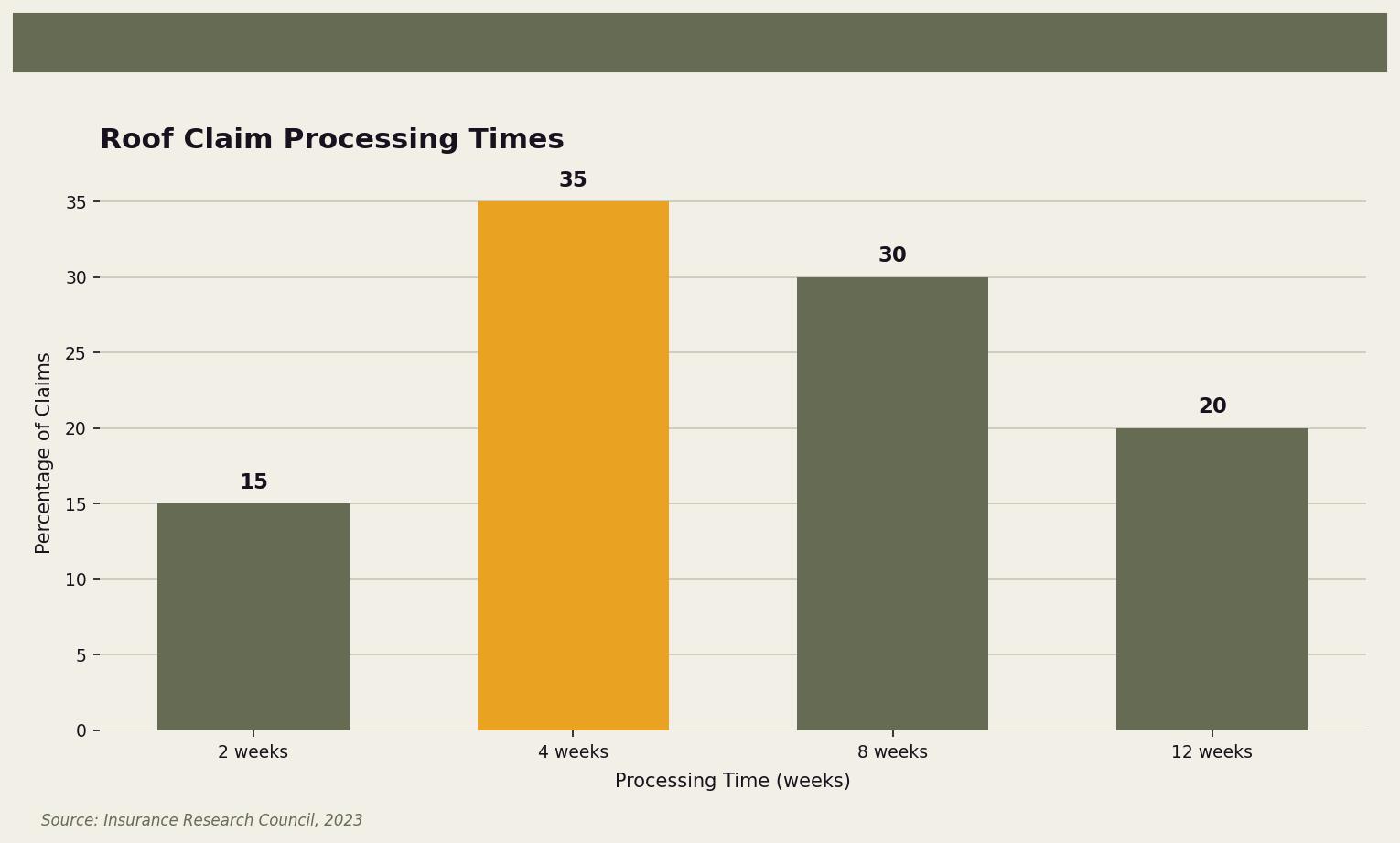

Once you file, you’re not done — you’re just getting started. According to a report by the Insurance Research Council, the average time to process a roof claim ranges from a couple of weeks to several months.

What affects that timeline?

- Severity of damage: Minor repairs process faster than full replacements

- Time of year: Post-storm seasons create backlogs (everyone files at once)

- Documentation quality: Clear photos and detailed notes speed things up

- Your insurer’s workload: Some companies are just slower than others

Here’s the insider tip: claims are typically processed on a first-come, first-served basis. File early after a storm, and you’re ahead of the rush. Wait three months, and you’re behind hundreds of other claims from the same weather event. Your adjuster is overworked, your contractor is booked out, and your timeline stretches from weeks to months.

Speed matters at every stage of this process.

Why Twin Cities Roofs Have It Harder Than Most

Living in Minnesota means accepting certain realities. Winters that test your patience. Mosquitoes that test your sanity. And weather patterns that absolutely punish residential roofs.

According to Climate Central, Minnesota experiences more than 100 freeze-thaw cycles annually. Think about what that means for your roof: water seeps into tiny cracks, freezes, expands, thaws, and repeats. Over and over. All winter long. It’s like your shingles are being slowly pried apart from the inside.

Add in our infamous ice dams, the hail that seems to find the Twin Cities every summer, and wind events that can rip shingles off in seconds — and you’ve got a recipe for roof damage that might not even be visible from the ground.

The numbers back this up. According to a 2023 survey by IBHS, Twin Cities residents are 30% more likely to file weather-related claims than the national average. We’re not imagining it. Our roofs really do take more abuse than most of the country.

This is exactly why staying on top of inspections and understanding your filing deadlines matters so much here. The question isn’t whether your roof will sustain damage — it’s when, and whether you’ll catch it in time.

Your Action Plan: What to Do Right Now

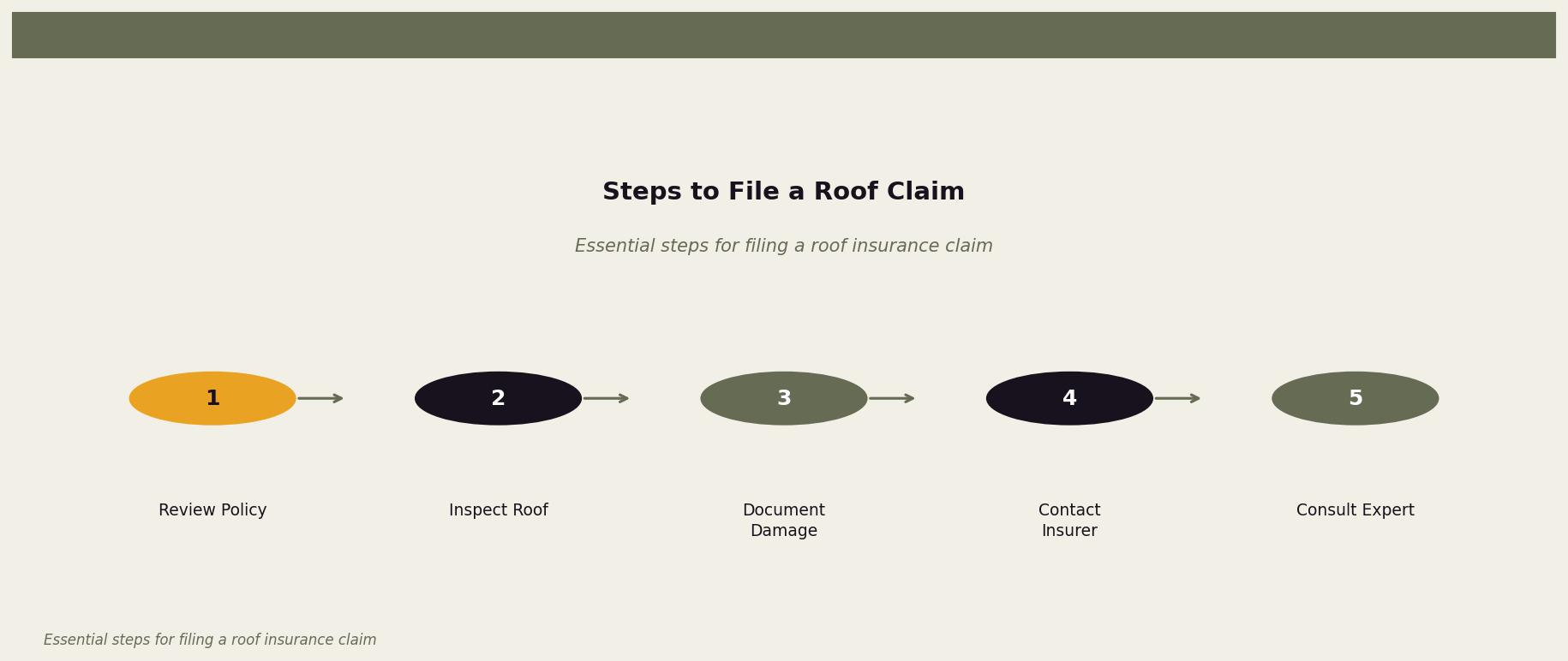

Okay, enough about the problem. Let’s talk solutions. Here’s exactly what you should do to protect yourself:

Step 1: Find Your Actual Deadline

Tonight, dig out your homeowner’s insurance policy (or log into your carrier’s website). Search for terms like “time limit,” “filing deadline,” or “notice of claim.” Write down the specific timeframe. If you can’t find it, call your agent tomorrow and ask directly: “How long do I have to file a roof claim after damage occurs?”

Step 2: Inspect Your Roof Regularly

You don’t need to climb up there yourself (please don’t). But you should:

- Walk around your property after every major storm and look for debris or visible damage

- Check your attic for water stains, daylight coming through, or moisture

- Schedule a professional inspection at least once a year — ideally in spring after winter damage and again in fall before the snow flies

Remember that stat about 73% of homeowners not inspecting their roof until there’s visible damage inside? Don’t be part of that statistic. By the time you see water stains on your ceiling, the damage has been happening for a while.

Step 3: Document Everything Immediately

The moment you notice potential damage:

- Take photos and videos from multiple angles (ground level is fine)

- Note the date and what weather event may have caused it

- Save any weather reports or news coverage of storms in your area

- Keep receipts if you need emergency repairs to prevent further damage

This documentation becomes your evidence. Insurance adjusters love clear photos and specific dates. Give them what they need to approve your claim.

Step 4: Contact Your Insurance Company Promptly

Don’t wait to see if the damage “gets worse.” Don’t wait until you’ve gotten repair estimates. File the initial claim as soon as you suspect damage. You can always provide additional documentation later — but you can’t un-miss a deadline.

Most carriers have 24/7 claims hotlines. Use them. Get a claim number. Get the process started.

Step 5: Work With a Local Roofing Expert

A good local roofer does more than just fix shingles. They can:

- Identify damage you might have missed

- Provide documentation that strengthens your claim

- Meet with your insurance adjuster to ensure nothing gets overlooked

- Help you understand what your policy actually covers

The key word here is “local.” Someone who knows Minnesota weather, understands Twin Cities insurance patterns, and will still be around next year if you need them.

Don’t Let a Deadline Cost You Thousands

Here’s the bottom line: your roof claim deadline is real, it’s probably shorter than you think, and missing it can cost you anywhere from $5,000 to $30,000 in repairs you’ll have to pay out of pocket.

But now you know. You know to check your policy. You know to inspect regularly. You know to document immediately and file quickly. You know that in the Twin Cities, roof damage isn’t a matter of “if” — it’s “when.”

Take 15 minutes this week to find your deadline and walk around your property. That small investment of time could save you a massive financial headache down the road.

Your roof is up there protecting your family every single day. Make sure your insurance is ready to protect it back — while you still have time.

Need a Roof Inspection? We’re Right Around the Corner.

We’re Owl Roofing — a family-owned company based right here in Shoreview, serving homeowners across the Twin Cities. No franchises, no storm chasers showing up from out of state, just your neighbors Tim, Bea, Noah, and Anya with 15+ years of combined experience fixing roofs exactly like yours.

If you’re not sure whether you have damage, or you’re worried about an upcoming claim deadline, give us a call. We’ll take a look, tell you exactly what we see, and help you figure out your next steps — no pressure, no runaround. We’ve helped dozens of homeowners navigate the insurance process, and we’re happy to do the same for you.

Call us at 651-977-6027 or visit owlroofing.com/ to schedule a free inspection.

Protect Your Nest.

📍 Owl Roofing Serves the Entire Twin Cities Metro

Andover · Anoka · Apple Valley · Arden Hills · Big Lake · Blaine · Bloomington · Brooklyn Center · Brooklyn Park · Burnsville · Champlin · Chanhassen · Chaska · Columbia Heights · Coon Rapids · Cottage Grove · Crystal · deephaven · Delano · Eagan · East Bethel · Eden Prairie · Excelsior · Farmington · Forest Lake · Fridley · Golden Valley · Ham Lake · Hastings · Hopkins · Hugo · Inver Grove Heights · Lake Elmo · Lakeville · Lino Lakes · Mahtomedi · Maplewood · Mendota Heights · Minneapolis · Minnetrista · Mound · Mounds View · New Brighton · New Hope · North Oaks · North St. Paul · Oak Grove · Oakdale · Plymouth · Prior Lake · Ramsey · Richfield · Robbinsdale · Rosemount · Roseville · Saint Paul · Savage · Shakopee · Shoreview · South St. Paul · St. Louis Park · St. Michael · St. Paul · Stillwater · Vadnais Heights · Victoria · Waconia · wayzata · West St. Paul · White Bear Lake · woodbury

Licensed Minnesota roofing contractor · Free inspections · 10-year workmanship warranty · Get a free estimate →