Recoverable Depreciation Explained for Roof Claims

12min Read

12min Read

Posted 12.03.2025

Posted 12.03.2025

That Insurance Check Looks Wrong—Here’s the $3,000 They’re Holding Back

You just survived a nasty Twin Cities hailstorm. Your roof took a beating. You filed the claim, did everything right—and then the insurance check arrives for $5,000 when your roof replacement costs $8,000. What gives? That missing $3,000 has a name: recoverable depreciation. And here’s the thing most homeowners don’t realize—you can get that money back. You just have to know how to ask for it.

Every year, we talk to Shoreview neighbors who left thousands of dollars on the table simply because nobody explained how their insurance claim actually works. That ends today.

The Problem: Insurance Math That Doesn’t Add Up

Here’s what happens after a Minnesota storm rips through your neighborhood. You call your insurance company. An adjuster shows up, pokes around your roof, and approves your claim. Victory, right?

Then the check arrives. And it’s… short. Way short.

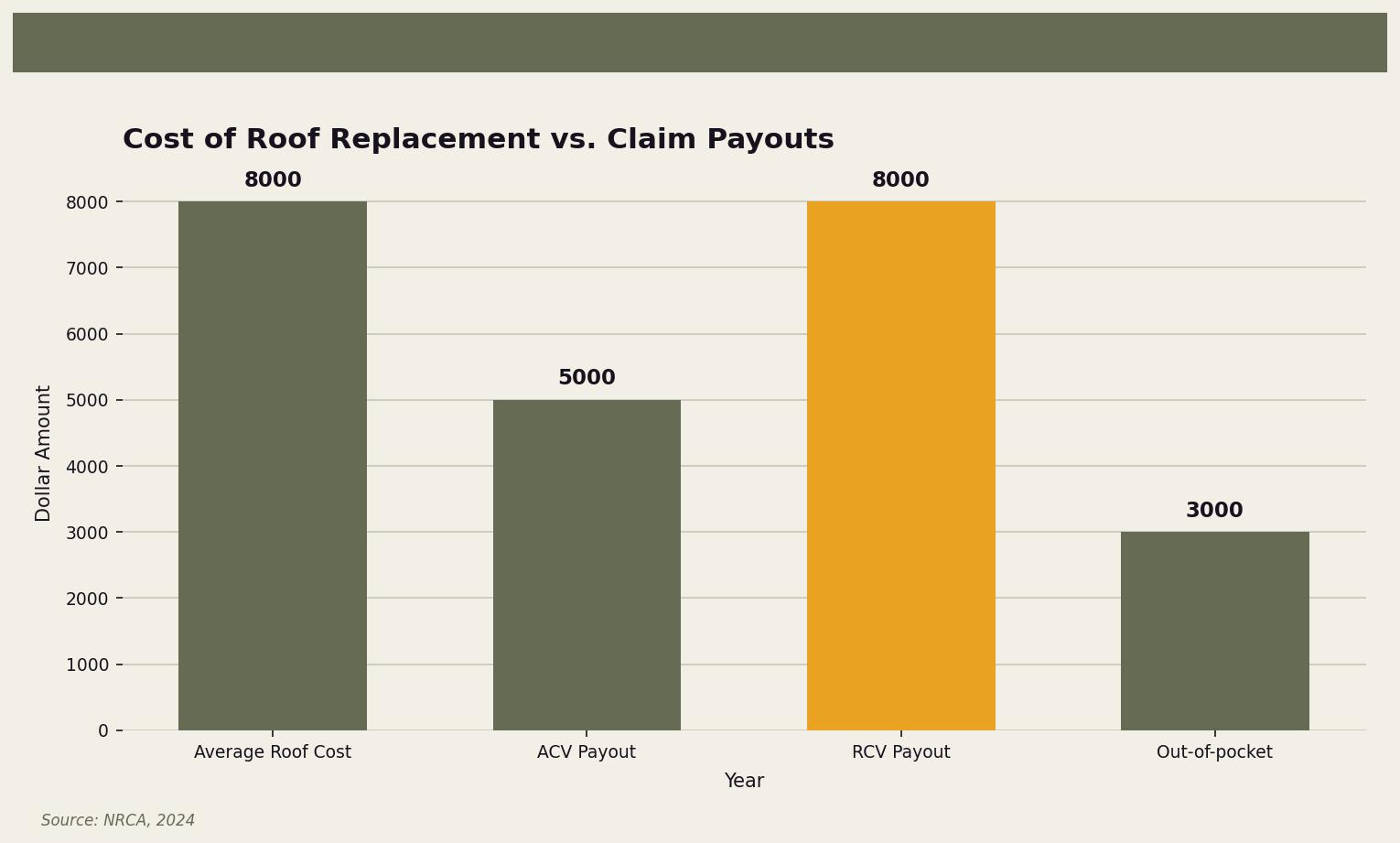

According to the National Association of Realtors, the average roof replacement runs around $8,000. But that first insurance check? It might only cover $5,000—or less. The insurance company isn’t scamming you (not exactly). They’re paying you something called Actual Cash Value, which factors in how old your roof is and how much it’s “depreciated.”

In plain English: they’re saying your 10-year-old roof isn’t worth what a new roof costs. So they cut you a smaller check and hold the rest hostage until you prove you actually fixed the roof.

That held-back portion? That’s your recoverable depreciation. And if you don’t understand it, you might never see that money.

Why This Hits Twin Cities Homeowners Especially Hard

Let’s be honest—Minnesota is rough on roofs. Our freeze-thaw cycles are brutal. Ice dams form every winter. Hail rolls through every summer. The National Roofing Contractors Association specifically calls out colder climates as high-risk zones for roof damage, and they’re not wrong.

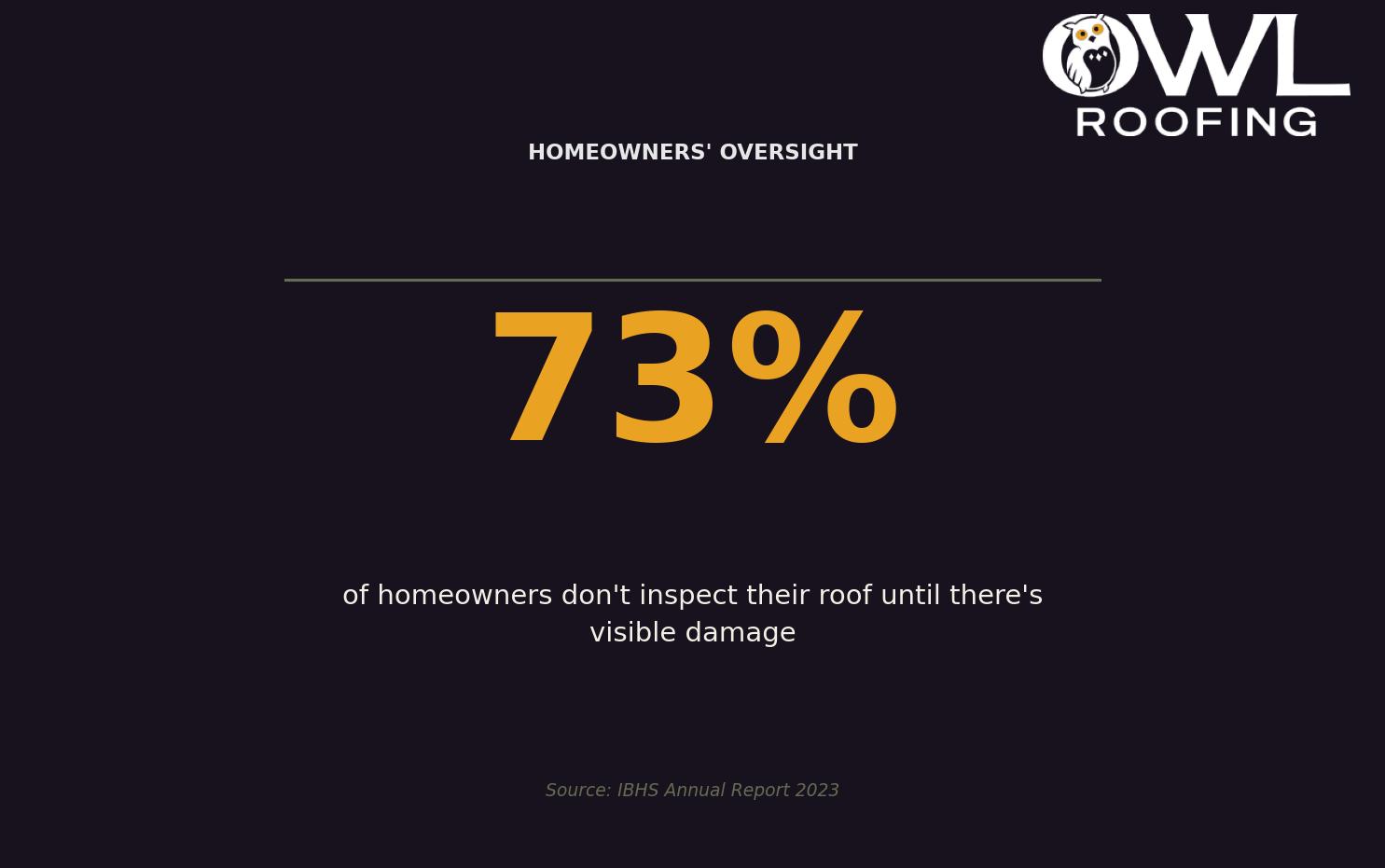

Here’s the kicker: the Insurance Institute for Business & Home Safety reports that 73% of homeowners don’t inspect their roof until damage is already visible. That means most folks are filing claims after years of unnoticed wear and tear—which gives insurance companies more room to depreciate your roof’s value.

And with property damage from weather events climbing every year (according to the Insurance Information Institute), more Twin Cities homeowners are dealing with this exact situation. You’re not alone. But you also can’t afford to leave money on the table.

What Recoverable Depreciation Actually Means (No Jargon, We Promise)

The Simple Version

When your insurance company calculates your claim, they look at two numbers:

Replacement Cost Value (RCV): What it actually costs to put a new roof on your house today. If your roof costs $8,000 to replace, your RCV is $8,000.

Actual Cash Value (ACV): What your old roof was “worth” at the moment it got damaged, minus depreciation for age and wear. If your roof was 10 years into a 20-year lifespan, they might calculate it’s only worth $5,000.

The difference between those two numbers—in this case, $3,000—is your depreciation. And if your policy includes recoverable depreciation (most do, but check yours), you can claim that $3,000 back after you complete the repairs.

Why Insurance Companies Do This

Insurance companies aren’t holding back money to be difficult (okay, maybe a little). The logic is: they want to make sure you actually fix your roof before paying out the full amount. They’ve been burned by homeowners who pocket the check and never make repairs. So they release funds in stages.

The problem? They don’t always explain this clearly. So homeowners see that first check, assume that’s all they’re getting, and either pay out of pocket for the difference or skip repairs altogether.

Neither option is good for your home—or your wallet.

ACV vs. RCV: Which Policy Do You Have?

This is where you need to pull out your actual insurance policy (or call your agent). Not all policies are created equal.

Actual Cash Value (ACV) Policies

Some policies only cover ACV—period. If you have one of these, depreciation is NOT recoverable. That smaller check is your final payout. These policies are cheaper for a reason: they leave you exposed when something goes wrong.

If you have an ACV-only policy and your roof is more than a few years old, you could be on the hook for thousands in out-of-pocket costs after storm damage.

Replacement Cost Value (RCV) Policies

RCV policies cover the full cost of replacing your roof with materials of similar kind and quality—no depreciation penalty. The Insurance Institute for Business & Home Safety specifically recommends RCV coverage for roofing policies because it offers genuinely comprehensive protection.

Most RCV policies work like this:

- First check: ACV amount (depreciated value)

- Second check: Recoverable depreciation (released after repairs are complete)

The catch? You have to actually complete the repairs AND file the paperwork to recover that depreciation. Miss a deadline or skip a step, and you forfeit the money.

A Story From Right Here in Shoreview

Last summer, a family a few blocks from Shoreview’s city park got hit by the same hailstorm that swept through half the metro. Dented gutters, cracked shingles, the whole deal. They filed their claim right away—did everything by the book.

Their insurance company approved a roof replacement. Great news. But that first check only covered about 60% of the actual cost. The adjuster mentioned something about “depreciation” and “a second payment later,” but it was confusing and rushed. The homeowners figured they’d gotten the short end of the stick and started budgeting to cover the gap themselves.

Fortunately, their roofer knew the drill. He walked them through the recoverable depreciation process, helped them understand the timeline, and made sure all the documentation was squared away after the job was done. Six weeks later, the second check arrived—for the full remaining balance.

No out-of-pocket costs. No financial stress. Just a new roof and an insurance system that actually worked the way it was supposed to.

That’s how it should go. But it only happens when someone explains the process clearly.

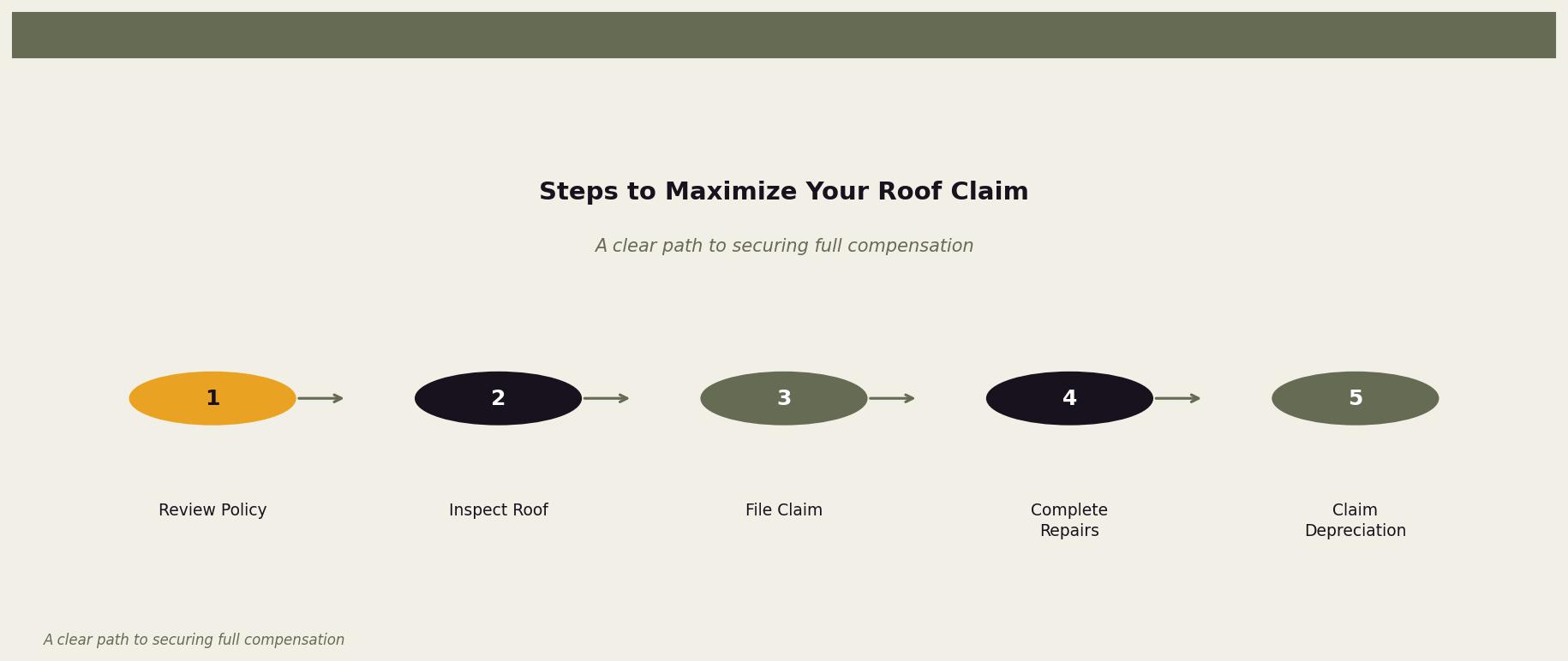

How to Actually Recover Your Depreciation (Step by Step)

Here’s your game plan for getting every dollar you’re owed:

Step 1: Review Your Policy Before You Need It

Don’t wait until a storm hits to figure out what you’re covered for. Pull out your homeowner’s policy today and look for these terms:

- Replacement Cost Value (RCV) — this is what you want

- Recoverable depreciation — confirms you can claim the held-back amount

- Time limits — most policies give you 180 days to a year to complete repairs and file for depreciation recovery

If your policy only covers ACV, call your insurance agent and ask about upgrading. The premium increase is usually modest compared to the protection you gain.

Step 2: Document Everything After Storm Damage

Take photos and videos of damage before any repairs start. Keep copies of your insurance correspondence, adjuster reports, and estimates. This paperwork protects you if there’s any dispute later.

Step 3: Get a Detailed Estimate from a Reputable Roofer

Work with a local roofing company that understands insurance claims inside and out. They should provide a line-item estimate that matches how insurance companies calculate costs. This isn’t the time for a vague “ballpark” number.

Step 4: Complete the Repairs Within Your Policy’s Deadline

This is crucial. If your policy gives you 180 days to complete repairs and claim recoverable depreciation, don’t wait until day 179. Weather delays, material shortages, contractor schedules—any of these can push you past the deadline. Start early.

Step 5: Submit Final Documentation and Request Depreciation Release

Once repairs are complete, your roofer should provide a certificate of completion and final invoice. Submit these to your insurance company along with a formal request to release your recoverable depreciation. Keep copies of everything you send.

Step 6: Follow Up (Politely but Persistently)

Insurance companies process a lot of claims. Yours might sit in a queue. Don’t be afraid to call and check on status. A friendly follow-up every week or two can speed things along.

Common Mistakes That Cost Homeowners Money

We’ve seen good people lose out on recoverable depreciation for avoidable reasons. Don’t let these happen to you:

- Missing the deadline: Every policy has a time limit for claiming recoverable depreciation. Mark it on your calendar the day you file your claim.

- Not completing all repairs: If your claim covers roof AND gutter damage, you need to repair both to recover full depreciation. Partial repairs = partial recovery.

- Poor documentation: If you can’t prove the work was done, the insurance company won’t release the funds. Get everything in writing.

- Working with an inexperienced contractor: Some roofers don’t understand insurance claims and leave homeowners to figure it out alone. Find someone who can guide you through the process.

- Assuming the first check is final: This is the biggest mistake of all. That initial ACV payment is just the beginning—not the end.

Why Regular Inspections Save You Headaches Later

Remember that stat about 73% of homeowners not inspecting their roof until damage is visible? Here’s why that matters for depreciation claims:

When an adjuster evaluates your roof, they’re looking at overall condition—not just storm damage. A well-maintained roof with documentation of regular inspections is harder to depreciate aggressively. A neglected roof with years of visible wear? That’s an easy target for a bigger depreciation deduction.

Getting your roof inspected annually (and especially after major storms) creates a paper trail that protects your claim value. It also catches small problems before they become expensive emergencies.

What to Do Right Now

Don’t wait for the next storm to hit. Here’s your action list:

- This week: Find your homeowner’s insurance policy and check for RCV coverage and recoverable depreciation terms.

- This month: Schedule a roof inspection if you haven’t had one in the past year (or since the last major storm).

- If you have pending damage: Get estimates from a reputable local roofer and start the claim process now. Time limits are real.

- If your policy is ACV-only: Call your insurance agent about upgrading to RCV coverage before the next hailstorm rolls through.

Ready to Make Sure You’re Fully Covered?

If your head is spinning a little right now, that’s totally normal. Insurance paperwork wasn’t designed to be homeowner-friendly. But you don’t have to navigate it alone.

At Owl Roofing, we’ve helped Shoreview neighbors and homeowners across the Twin Cities recover every dollar they’re entitled to after storm damage. We’ve seen every version of this story—the confusing adjuster visits, the short first checks, the missed deadlines. And we’ve walked families through the process from first inspection to final depreciation recovery.

We’re a local, family-owned company (Tim & Bea Brown, Noah & Anya Bergland—you might have seen us at the hardware store or the coffee shop). Not a franchise. Not storm chasers who disappear after the job. Your neighbors, looking out for your home the same way we’d look out for our own.

If you’ve got roof damage, questions about your insurance claim, or just want someone to take a look before the next storm season, give us a call at 651-977-6027 or visit owlroofing.com/. We’ll tell you exactly what your roof needs—no pressure, no runaround.

Protect Your Nest.

📍 Owl Roofing Serves the Entire Twin Cities Metro

Andover · Anoka · Apple Valley · Arden Hills · Big Lake · Blaine · Bloomington · Brooklyn Center · Brooklyn Park · Burnsville · Champlin · Chanhassen · Chaska · Columbia Heights · Coon Rapids · Cottage Grove · Crystal · deephaven · Delano · Eagan · East Bethel · Eden Prairie · Excelsior · Farmington · Forest Lake · Fridley · Golden Valley · Ham Lake · Hastings · Hopkins · Hugo · Inver Grove Heights · Lake Elmo · Lakeville · Lino Lakes · Mahtomedi · Maplewood · Mendota Heights · Minneapolis · Minnetrista · Mound · Mounds View · New Brighton · New Hope · North Oaks · North St. Paul · Oak Grove · Oakdale · Plymouth · Prior Lake · Ramsey · Richfield · Robbinsdale · Rosemount · Roseville · Saint Paul · Savage · Shakopee · Shoreview · South St. Paul · St. Louis Park · St. Michael · St. Paul · Stillwater · Vadnais Heights · Victoria · Waconia · wayzata · West St. Paul · White Bear Lake · woodbury

Licensed Minnesota roofing contractor · Free inspections · 10-year workmanship warranty · Get a free estimate →