Roof Financing Options How to Pay for a New Roof

11min Read

11min Read

Posted 11.12.2025

Posted 11.12.2025

The $15,000 Question Nobody Wants to Ask

Your roof is leaking, and you just got the estimate: $12,000 to $18,000 for a full replacement. Your stomach drops. You knew this day would come — those curling shingles weren’t getting any younger — but where exactly is that kind of money supposed to come from? Here’s the truth most Twin Cities homeowners don’t realize: you have more options than you think, and some of them won’t cost you a dime in interest.

We’re going to walk through every realistic way to pay for a new roof, from the obvious to the overlooked. No gimmicks, no “just put it on a credit card” nonsense. By the end, you’ll have a clear plan to protect your home without wrecking your finances.

Why You Can’t Afford to Wait (And the Numbers Prove It)

Let’s talk stakes. In the Twin Cities, your roof isn’t just a nice-to-have — it’s the only thing standing between your family and some of the harshest weather in the country. The U.S. Census Bureau reports that Minnesota experiences over 50 freeze-thaw cycles annually. That’s 50+ times per year where water seeps into cracks, freezes, expands, and turns small problems into big ones.

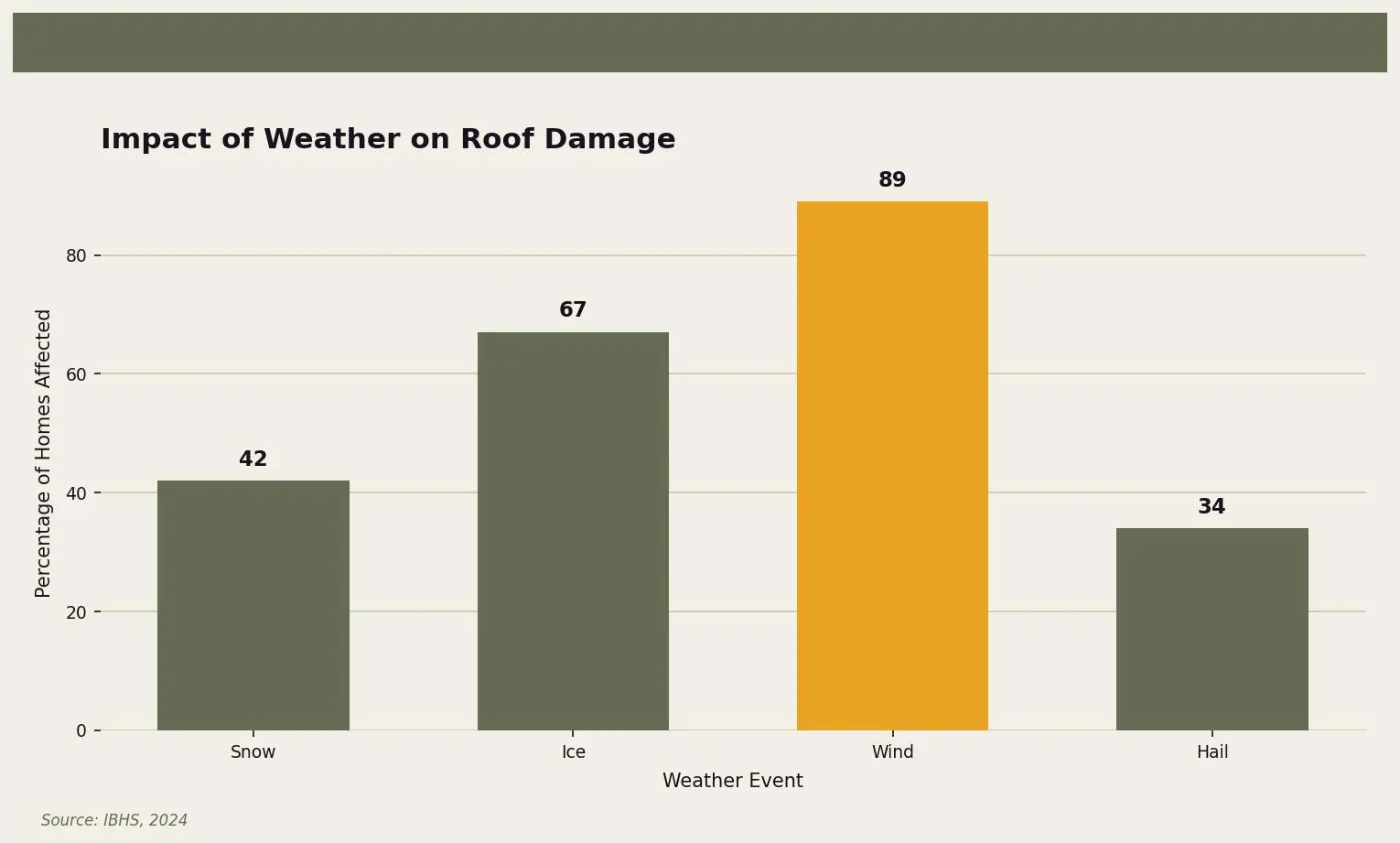

The Insurance Institute for Business & Home Safety (IBHS) found that more than 40% of homes suffer roof damage due to severe weather conditions. If you’re putting off a replacement because of cost, that damaged roof is working against you every single day — raising your heating bills, inviting mold, and quietly destroying the structure underneath.

But here’s the flip side: a new roof isn’t just an expense. It’s an investment. According to the National Association of Realtors (NAR), a new roof can recover more than 60% of its cost in added home value. If you’re even thinking about selling in the next decade, that math matters.

So yes, a roof replacement is expensive. But the cost of waiting? That’s often higher.

Your Roof Financing Options: The Full Breakdown

Not all financing is created equal. Some options make sense for certain situations, others are traps dressed up as convenience. Let’s break down what’s actually available to Twin Cities homeowners.

Option 1: Personal Savings and Emergency Funds

If you’ve got the cash sitting in an emergency fund, this is the cleanest path forward. No interest payments. No credit checks. No monthly bills to juggle. You pay once, it’s done, and you move on with your life.

The catch? Using your emergency fund for a roof leaves you exposed if something else goes wrong. Car breaks down? Medical bill shows up? You’re back to square one without a safety net.

Best for: Homeowners with savings beyond their core emergency fund — money they’ve specifically set aside for home repairs or large expenses.

Pro tip: Some homeowners split the difference. They pay 50% from savings and finance the rest, keeping a cushion while still reducing interest costs.

Option 2: Home Equity Loans

This is one of the most popular choices for major home repairs, and for good reason. A home equity loan lets you borrow against the value you’ve built in your home, typically at interest rates much lower than credit cards or personal loans.

According to the National Roofing Contractors Association (NRCA), homeowners often favor this option for significant repairs like roof replacement because the rates are competitive and the terms are predictable — fixed monthly payments over a set period.

The catch? Your home is the collateral. If you can’t make payments, you could face foreclosure. That’s not a scare tactic; it’s just the reality of secured debt.

Best for: Homeowners with significant equity built up, stable income, and confidence in their ability to make consistent payments.

Current landscape: As of 2024, home equity loan rates hover between 7-9% for most borrowers with good credit — significantly better than the 20%+ you’d pay on a credit card.

Option 3: Home Equity Line of Credit (HELOC)

Similar to a home equity loan, but with more flexibility. A HELOC works like a credit card backed by your home — you get approved for a maximum amount and draw from it as needed.

Why this matters for roofing: If you’re not sure of the final cost (maybe you want repairs to the gutters or soffit while the crew is up there), a HELOC lets you handle additional work without applying for more financing.

The catch? HELOCs typically have variable interest rates. What starts at 7% could climb to 10% or higher if rates rise. Also, that same foreclosure risk applies.

Best for: Homeowners who want flexibility and are comfortable managing variable payments.

Option 4: Personal Loans (Roofing Loans)

Many banks and credit unions offer personal loans specifically marketed for home improvements. These are unsecured — meaning your home isn’t on the line — but that safety comes at a cost: higher interest rates, usually between 8-15% depending on your credit score.

The NRCA suggests comparing rates and terms from multiple lenders to find the best deal. Don’t just walk into your bank and accept the first offer. Online lenders, local credit unions, and even some contractors offer competing options.

The catch? Higher rates mean higher total cost over time. A $15,000 roof financed at 12% over five years costs you nearly $5,000 in interest alone.

Best for: Homeowners who don’t have enough equity for a home equity loan, or who aren’t comfortable using their home as collateral.

Option 5: Contractor Financing

Some roofing companies offer in-house financing or partner with financial institutions to provide payment plans right at the time of your estimate. Convenient? Absolutely. But convenience often comes with strings attached.

What to watch for:

- Promotional rates that skyrocket after the intro period

- Deferred interest plans (if you don’t pay in full by the deadline, you owe ALL the interest retroactively)

- Higher rates than you’d get shopping around independently

The catch? These programs can be great — or they can be traps. Always read every line of the agreement. Ask exactly what happens if you miss a payment or don’t pay off the balance in time.

Best for: Homeowners who’ve read the fine print, understand the terms, and find the convenience worth any rate premium.

Option 6: Credit Cards (Use With Extreme Caution)

Can you put a roof on a credit card? Technically, yes — some contractors accept them. Should you? Almost never.

Credit card interest rates average over 20%. A $15,000 roof paid off over three years at 22% APR would cost you more than $5,500 in interest. That’s an entire bathroom renovation worth of money going straight to the bank.

The one exception: If you have a 0% APR promotional card AND can pay off the full balance before the promotion ends, this could work in your favor. But you need iron discipline and a clear payoff plan.

Best for: Almost nobody. This is a last resort, not a strategy.

Option 7: Government Programs and Incentives

Here’s what most homeowners don’t know: there may be programs that can help, especially if you’re making energy-efficient upgrades.

- FHA Title I Loans: Government-backed loans for home improvements, available even with lower credit scores

- Energy-efficient roofing credits: Some roofing materials (like ENERGY STAR-rated products) may qualify for tax credits

- State and local programs: Minnesota occasionally offers weatherization assistance or low-interest home improvement loans for qualifying homeowners

Best for: Homeowners willing to do the research and paperwork. These programs exist — they’re just not well-advertised.

The Twin Cities Timing Factor

Here in Minnesota, when you finance matters almost as much as how you finance. Our roofing season runs roughly April through October. Try to get your project scheduled in the shoulder seasons (early spring or late fall) and you might find more flexibility from contractors — and more time to get your financing squared away.

What you don’t want is to discover a leak in January and scramble for emergency financing while your living room turns into a splash zone. That’s when bad financial decisions get made.

The smart move? Get a roof inspection now, while everything’s dry and calm. Know what you’re dealing with, and give yourself time to choose the right financing path on your terms — not in a crisis.

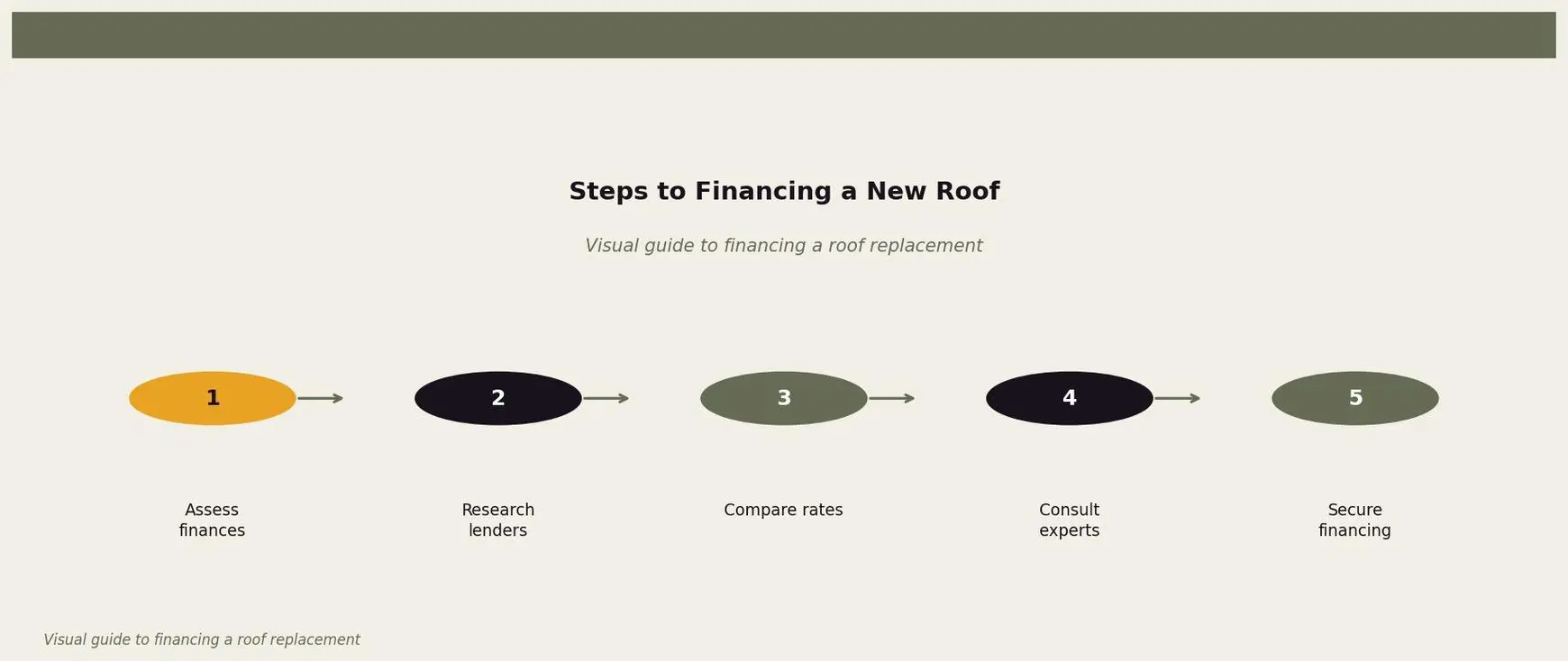

Your 5-Step Action Plan

Enough theory. Here’s exactly what to do next:

Step 1: Know your numbers. Check your credit score (free at annualcreditreport.com), review your savings, and calculate what monthly payment you could comfortably handle. Be honest with yourself.

Step 2: Get a professional roof inspection. Before you finance anything, know exactly what you’re dealing with. A good roofer will tell you whether you need a full replacement, repairs, or if you’ve got a few more years.

Step 3: Shop multiple lenders. Don’t accept the first offer. Compare at least three options — your bank, a credit union, and an online lender. Even a 1% difference in interest rate saves hundreds over the loan term.

Step 4: Read every contract. Especially contractor financing. Ask about prepayment penalties, what happens if you pay late, and whether the rate is fixed or variable.

Step 5: Make your decision and act. Once you’ve done the research, don’t second-guess yourself into another Minnesota winter with a failing roof. Commit to the plan and protect your home.

What Happens If You Don’t Act

Let’s be real about the alternative. That “minor” leak you’ve been ignoring? Here’s where it leads:

- Water damage spreads to insulation, drywall, and framing

- Mold develops (remediation costs $1,500 to $9,000 on average)

- Structural damage that turns a $15,000 roof job into a $40,000 renovation

- Insurance claims get denied because the damage was “preventable neglect”

- Home value drops — buyers walk away from inspection nightmares

A new roof is expensive. But it’s nothing compared to the cost of a damaged home. The financing options exist specifically so you can act before small problems become disasters.

Talk to Your Neighbors at Owl Roofing

If you’re staring down a roof replacement and feeling overwhelmed by the options, we get it. We’ve sat at plenty of kitchen tables in Shoreview and across the Twin Cities, walking homeowners through exactly these decisions. Tim, Bea, Noah, and Anya started Owl Roofing because our neighbors deserve straight answers — not sales pitches.

We’ll inspect your roof, tell you honestly what it needs (and what it doesn’t), and help you understand your financing options without any pressure. That’s just how neighbors should treat each other.

Give us a call at 651-977-6027 or visit owlroofing.com/ to schedule a free inspection. We’re right here in Shoreview, serving the entire Twin Cities metro — and we’re not going anywhere.

Protect Your Nest.

📍 Owl Roofing Serves the Entire Twin Cities Metro

Andover · Anoka · Apple Valley · Arden Hills · Big Lake · Blaine · Bloomington · Brooklyn Center · Brooklyn Park · Burnsville · Champlin · Chanhassen · Chaska · Columbia Heights · Coon Rapids · Cottage Grove · Crystal · deephaven · Delano · Eagan · East Bethel · Eden Prairie · Excelsior · Farmington · Forest Lake · Fridley · Golden Valley · Ham Lake · Hastings · Hopkins · Hugo · Inver Grove Heights · Lake Elmo · Lakeville · Lino Lakes · Mahtomedi · Maplewood · Mendota Heights · Minneapolis · Minnetrista · Mound · Mounds View · New Brighton · New Hope · North Oaks · North St. Paul · Oak Grove · Oakdale · Plymouth · Prior Lake · Ramsey · Richfield · Robbinsdale · Rosemount · Roseville · Saint Paul · Savage · Shakopee · Shoreview · South St. Paul · St. Louis Park · St. Michael · St. Paul · Stillwater · Vadnais Heights · Victoria · Waconia · wayzata · West St. Paul · White Bear Lake · woodbury

Licensed Minnesota roofing contractor · Free inspections · 10-year workmanship warranty · Get a free estimate →